Submit Request

Rest assured, your privacy is paramount to us. The information you provide will be treated with the utmost confidentiality and used exclusively for investment-related communications. We will never share your data with third parties without your consent.

Thank you for considering Atrani Capital for your investment needs. We look forward to connecting with you soon to explore the wealth of opportunities that can benefit us both.

Atrani Monthly magazine

Investors journey - 4, May-June 2026

Good afternoon, dear readers,

We are pleased to present our new issue, featuring three insightful articles:

We hope you find it interesting and valuable. We would be happy to hear your feedback — feel free to write to us at clients@atranicapital.com.

We are pleased to present our new issue, featuring three insightful articles:

- Mega AI IPOs Are Turning Into the Market’s Next Stress Test

- SpaceX’s First Two Weeks: AI Premium, Retail Frenzy, and the Return of Gravity

- June 2026 Bank of America Global Fund Manager Survey

We hope you find it interesting and valuable. We would be happy to hear your feedback — feel free to write to us at clients@atranicapital.com.

Mega AI IPOs Are Turning Into the Market’s Next Stress Test

SpaceX’s IPO demand appears to be extremely strong. According to Bloomberg, the deal is already significantly oversubscribed, with several institutional investors reportedly placing orders for about $10 billion or more each. Banks are expected to close institutional order books after Wednesday’s market close, ahead of pricing on June 11 and trading the following day. Retail demand is also part of the story: SpaceX is reportedly allocating as much as 30% of the offering to retail investors, an unusually large share for a deal of this size.

But SpaceX is no longer a standalone event. Anthropic has confidentially submitted draft IPO paperwork and could list as soon as this fall, potentially ahead of OpenAI. OpenAI has also filed confidentially, joining a pipeline of AI-linked mega-IPOs with a combined reported private valuation of roughly $3.6 trillion. The timing is remarkable: three of the most important private AI companies may be preparing to enter public markets within the same window, just as investors are still debating whether the AI capex boom is creating durable cash flows or simply pulling future demand forward.

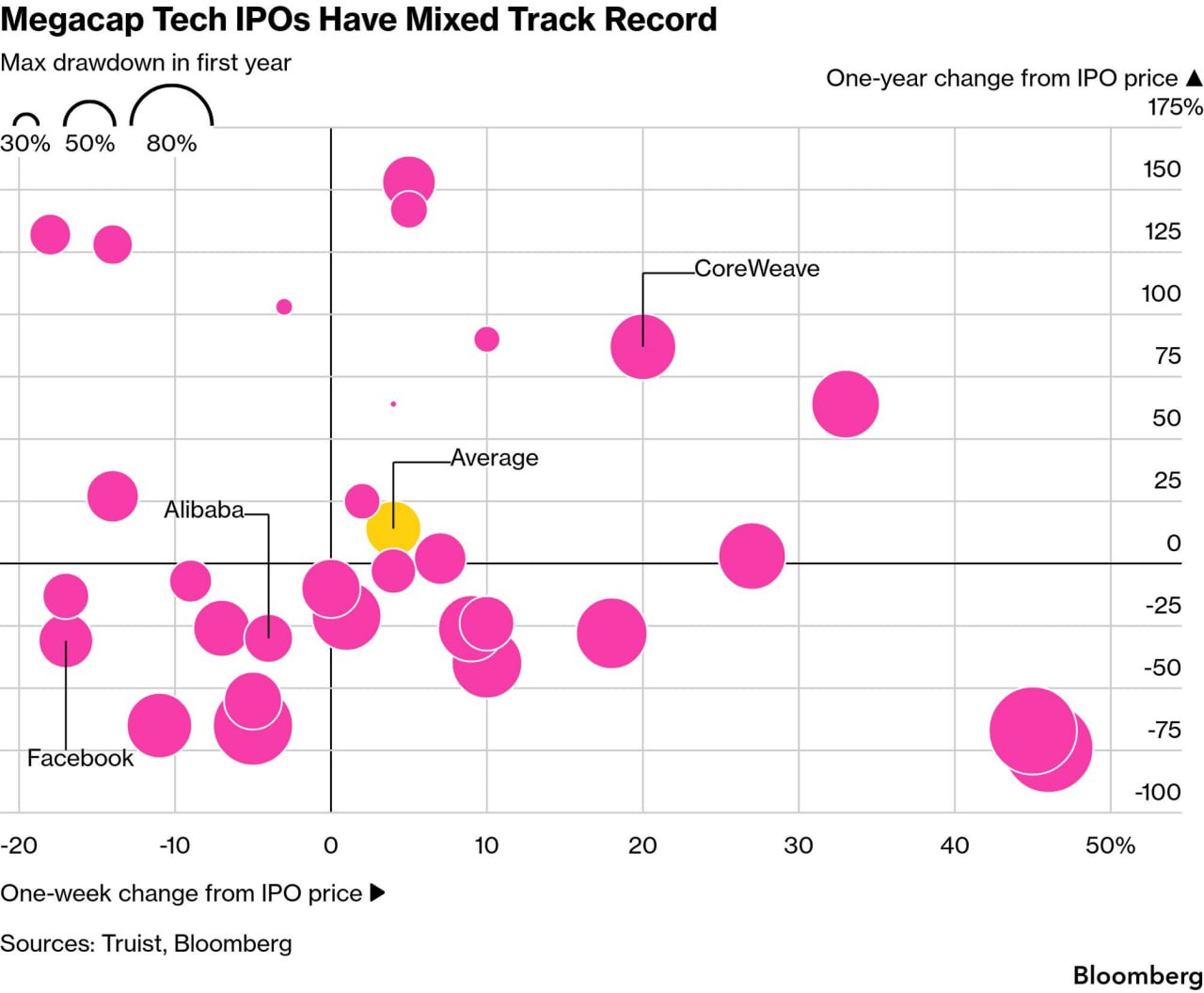

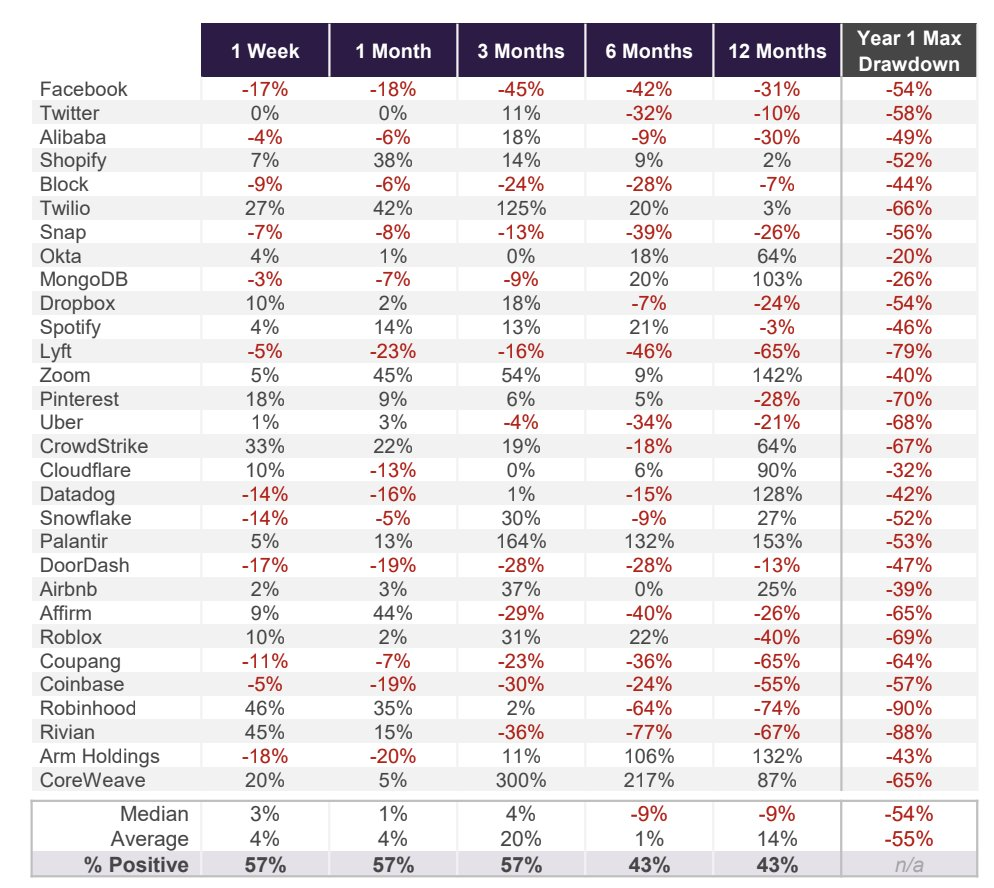

History argues for separating first-day excitement from long-term returns. Several datasets on large and technology IPOs point to the same pattern: scarcity and demand can drive strong early trading, but performance often deteriorates once valuation, lockups, liquidity and fundamentals become more important. Bloomberg, citing Truist Wealth, noted that 30 major technology IPOs over the past 15 years suffered an average maximum first-year drawdown of 55%, with median returns of -9% after both six and twelve months. Barron’s, citing Jefferies, reported a similar pattern for IPOs above $10 billion in market value: average gains were strong in the first week, but much less impressive by the end of the first year. Simply put, the first trade is often about access and enthusiasm; the first year is when price discipline starts to matter.

That is especially relevant for SpaceX. Morningstar’s latest analysis values the company at only $63 per share, a 53% discount to the proposed $135 IPO price. Its scenario work is striking: only the most optimistic “Moonshot” case, where Starship becomes rapidly reusable and orbital data centers scale commercially, comes close to the IPO price, with an estimated value of $154 per share — and Morningstar assigns that scenario just a 7% probability. Its base math treats much of the IPO premium as an option on future projects rather than value supported by today’s businesses.

The broader lesson is not that investors should ignore these IPOs. Meta fell more than 30% in its first year after listing and later rose more than 1,400% from its IPO price. Tesla was volatile and underperformed the S&P 500 after its first year, yet eventually became one of the great wealth-creation stories of the market. Great companies can still be poor purchases if bought at peak excitement, especially when initial floats are small and later lockup expirations bring more supply.

So the coming AI IPO wave may become one of the biggest tests of public-market discipline in years. SpaceX, Anthropic and OpenAI are not ordinary listings; they are companies that could reshape entire industries. But their IPOs will also test whether investors can separate strategic importance from price. The first trade may be about scarcity. The long-term return will depend on whether these companies can turn huge AI narratives into durable revenue, margins and free cash flow.

But SpaceX is no longer a standalone event. Anthropic has confidentially submitted draft IPO paperwork and could list as soon as this fall, potentially ahead of OpenAI. OpenAI has also filed confidentially, joining a pipeline of AI-linked mega-IPOs with a combined reported private valuation of roughly $3.6 trillion. The timing is remarkable: three of the most important private AI companies may be preparing to enter public markets within the same window, just as investors are still debating whether the AI capex boom is creating durable cash flows or simply pulling future demand forward.

History argues for separating first-day excitement from long-term returns. Several datasets on large and technology IPOs point to the same pattern: scarcity and demand can drive strong early trading, but performance often deteriorates once valuation, lockups, liquidity and fundamentals become more important. Bloomberg, citing Truist Wealth, noted that 30 major technology IPOs over the past 15 years suffered an average maximum first-year drawdown of 55%, with median returns of -9% after both six and twelve months. Barron’s, citing Jefferies, reported a similar pattern for IPOs above $10 billion in market value: average gains were strong in the first week, but much less impressive by the end of the first year. Simply put, the first trade is often about access and enthusiasm; the first year is when price discipline starts to matter.

That is especially relevant for SpaceX. Morningstar’s latest analysis values the company at only $63 per share, a 53% discount to the proposed $135 IPO price. Its scenario work is striking: only the most optimistic “Moonshot” case, where Starship becomes rapidly reusable and orbital data centers scale commercially, comes close to the IPO price, with an estimated value of $154 per share — and Morningstar assigns that scenario just a 7% probability. Its base math treats much of the IPO premium as an option on future projects rather than value supported by today’s businesses.

The broader lesson is not that investors should ignore these IPOs. Meta fell more than 30% in its first year after listing and later rose more than 1,400% from its IPO price. Tesla was volatile and underperformed the S&P 500 after its first year, yet eventually became one of the great wealth-creation stories of the market. Great companies can still be poor purchases if bought at peak excitement, especially when initial floats are small and later lockup expirations bring more supply.

So the coming AI IPO wave may become one of the biggest tests of public-market discipline in years. SpaceX, Anthropic and OpenAI are not ordinary listings; they are companies that could reshape entire industries. But their IPOs will also test whether investors can separate strategic importance from price. The first trade may be about scarcity. The long-term return will depend on whether these companies can turn huge AI narratives into durable revenue, margins and free cash flow.

SpaceX’s First Two Weeks: AI Premium, Retail Frenzy, and the Return of Gravity

SpaceX’s first two weeks as a public company were not a normal post-IPO trading period. They were a stress test of one of the most complicated investment stories the public market has ever been asked to price.

The company came public at $135 per share, rallied sharply in its first sessions, and then gave back a meaningful part of the move. That reversal does not make the IPO a failure. SpaceX still trades above its offer price. But it does mark the end of the easiest part of the story: the initial scarcity trade.

The company came public at $135 per share, rallied sharply in its first sessions, and then gave back a meaningful part of the move. That reversal does not make the IPO a failure. SpaceX still trades above its offer price. But it does mark the end of the easiest part of the story: the initial scarcity trade.

The harder question now is what investors actually own. SpaceX is no longer being valued only as a launch company. Public shareholders are buying a dominant space business, Starlink’s satellite-connectivity cash flows, a newly enlarged AI-infrastructure platform, Elon Musk’s control premium, and a future stream of index and retail demand — all in one ticker.

In rocketry, Max Q is the moment of maximum aerodynamic stress, when a launch vehicle faces the greatest pressure during ascent. For SpaceX stock, Max Q may not have been the first day of trading. It may come over the next several quarters, as the opening scarcity premium fades and the market has to absorb lockup releases, AI capital needs, public earnings scrutiny, and the reality of valuation.

That is the right way to read the IPO. The first rally was liftoff. The next phase is price discovery.

In rocketry, Max Q is the moment of maximum aerodynamic stress, when a launch vehicle faces the greatest pressure during ascent. For SpaceX stock, Max Q may not have been the first day of trading. It may come over the next several quarters, as the opening scarcity premium fades and the market has to absorb lockup releases, AI capital needs, public earnings scrutiny, and the reality of valuation.

That is the right way to read the IPO. The first rally was liftoff. The next phase is price discovery.

1. The IPO was designed as a funding event, not a normal price-discovery exercise

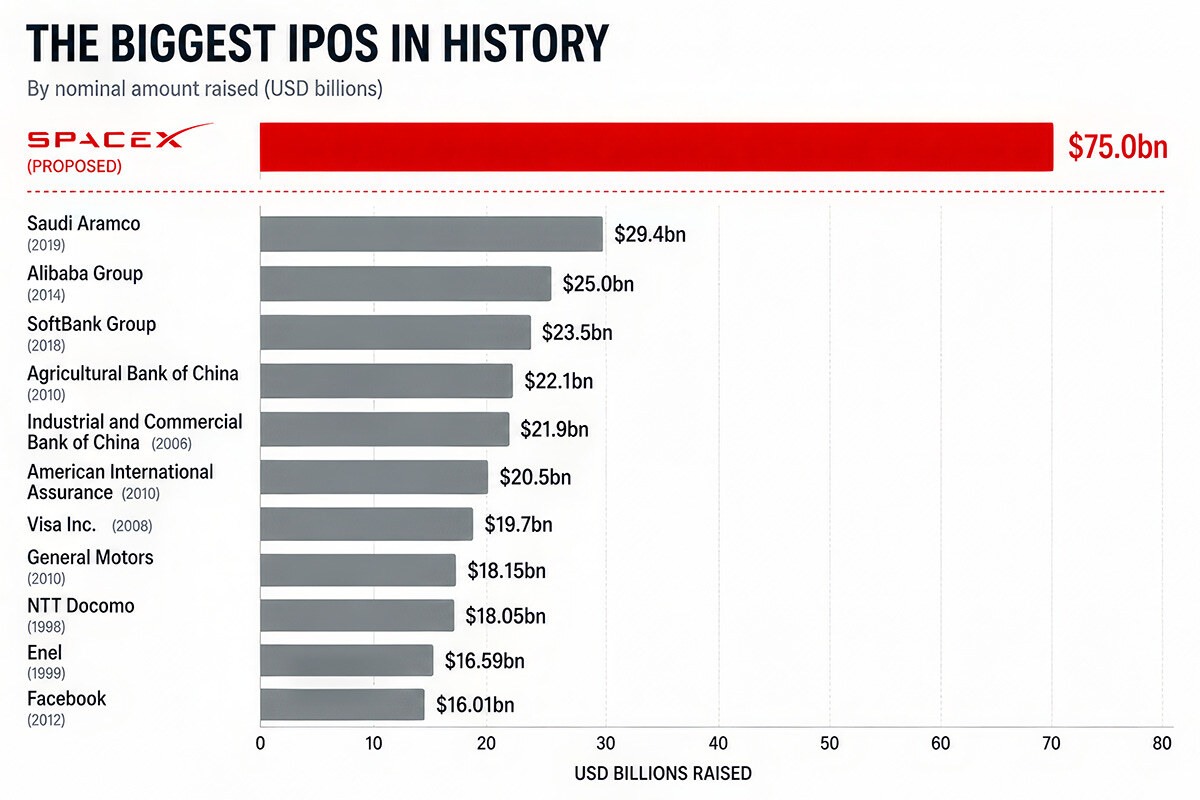

The offering was unusually direct. SpaceX set a single expected price of $135 per share, rather than a traditional price range. Analysts described it as a “take-it-or-leave-it” structure that left less room for conventional bookbuilding theater. At that price, the initial 555,555,555 share sale implied roughly $75 billion of gross proceeds and a valuation near $1.75 trillion.

The company’s prospectus framed the proceeds as growth capital: AI compute infrastructure, launch infrastructure, launch vehicles, satellite constellation capacity, and general corporate purposes. The document also reserved 5% of shares for a directed share program and made clear that SpaceX would be a controlled company after the IPO.

That matters. This was not merely a liquidity event for early investors. It was a balance-sheet event for a company that became much more capital intensive once the xAI/X combination turned SpaceX and Starlink into a broader AI-infrastructure story.

The company’s prospectus framed the proceeds as growth capital: AI compute infrastructure, launch infrastructure, launch vehicles, satellite constellation capacity, and general corporate purposes. The document also reserved 5% of shares for a directed share program and made clear that SpaceX would be a controlled company after the IPO.

That matters. This was not merely a liquidity event for early investors. It was a balance-sheet event for a company that became much more capital intensive once the xAI/X combination turned SpaceX and Starlink into a broader AI-infrastructure story.

(Source: The Investor Standard)

2. SpaceX is now a space, connectivity and AI story

The most important financial fact in the prospectus is that SpaceX is already a real business — but not all parts of it are equally real, equally profitable, or equally mature.

In 2025, SpaceX generated $18.674 billion of consolidated revenue, up 33.2% from 2024, but reported a $4.937 billion net loss. The income statement shows the tension: huge revenue growth, huge R&D growth, and a newly enlarged AI segment that changes the consolidated profile.

The segment breakdown is the key:

In 2025, SpaceX generated $18.674 billion of consolidated revenue, up 33.2% from 2024, but reported a $4.937 billion net loss. The income statement shows the tension: huge revenue growth, huge R&D growth, and a newly enlarged AI segment that changes the consolidated profile.

The segment breakdown is the key:

- SpaceX’s Space segment generated $4.086 billion of 2025 revenue, lost $657 million from operations, and produced $653 million of segment adjusted EBITDA. That operating loss included roughly $3.0 billion of R&D tied to Starship.

- The Connectivity segment, essentially Starlink, is the financial engine. It produced $11.387 billion of 2025 revenue, $4.423 billion of operating income, and $7.168 billion of segment adjusted EBITDA. That is why the market does not treat SpaceX like a speculative rocket startup. Starlink is already a scaled, profitable infrastructure business.

- The new AI segment is the opposite: large, fast-growing, and deeply loss-making. In 2025, it generated $3.201 billion of revenue, lost $6.355 billion from operations, and consumed $12.727 billion of capital expenditures.

3. The roadshow was not just about space. It was an AI pitch built on a space monopoly

The roadshow materials were cinematic: Mars, launch plumes, orbital infrastructure, and the promise of “building the infrastructure of the future.” But the most important part of the pitch was not the imagery. It was the reframing of SpaceX from a rocket-and-satellite company into an integrated space, connectivity and AI platform.

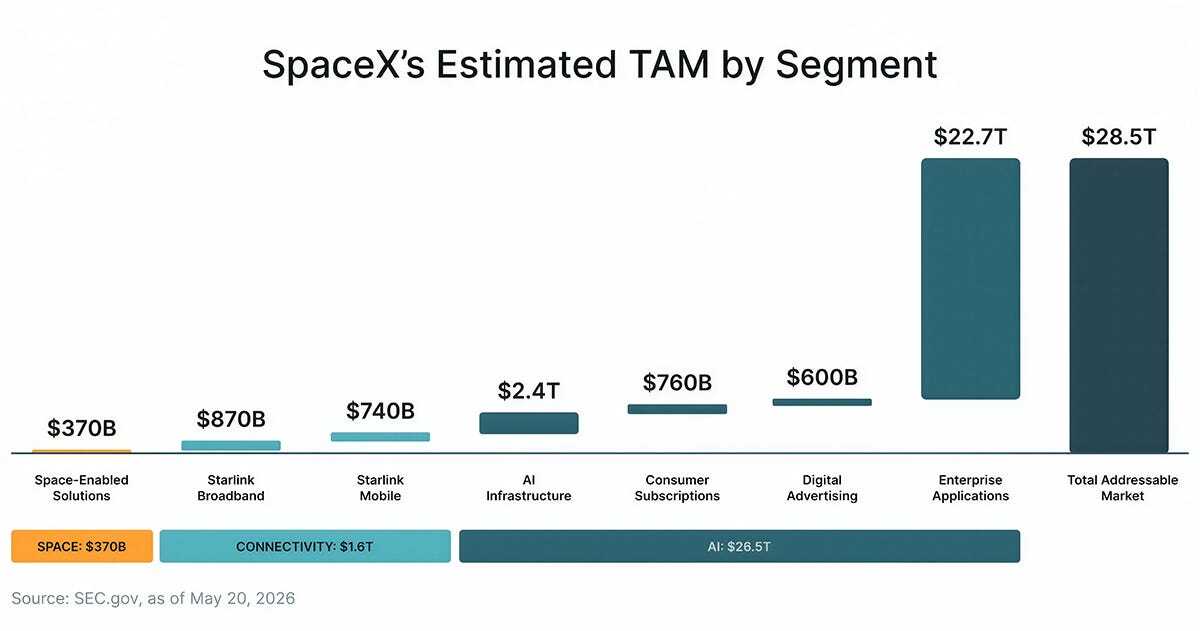

The roadshow’s own numbers made that clear. SpaceX presented a near-term addressable market of roughly $5.7 trillion, split across space-enabled solutions, Starlink broadband, Starlink mobile, AI infrastructure, consumer subscriptions and digital advertising. Even in this nearer-term framing, AI was already the largest block: $2.4 trillion for AI infrastructure, $760 billion for consumer subscriptions and $600 billion for digital advertising — together about $3.8 trillion, compared with $1.6 trillion for connectivity and $370 billion for space-enabled solutions.

The longer-term framing was even more aggressive. SpaceX was marketing itself around a $28.5 trillion total addressable market, with AI accounting for $26.5 trillion, or about 93% of the total. Enterprise applications were the largest part of that opportunity. In other words, the IPO story was not primarily that SpaceX could launch more rockets. It was that SpaceX could use its launch advantage, Starlink cash flows, xAI models, X data, compute infrastructure and eventually orbital data centers to compete for one of the largest profit pools in the AI economy.

The roadshow’s own numbers made that clear. SpaceX presented a near-term addressable market of roughly $5.7 trillion, split across space-enabled solutions, Starlink broadband, Starlink mobile, AI infrastructure, consumer subscriptions and digital advertising. Even in this nearer-term framing, AI was already the largest block: $2.4 trillion for AI infrastructure, $760 billion for consumer subscriptions and $600 billion for digital advertising — together about $3.8 trillion, compared with $1.6 trillion for connectivity and $370 billion for space-enabled solutions.

The longer-term framing was even more aggressive. SpaceX was marketing itself around a $28.5 trillion total addressable market, with AI accounting for $26.5 trillion, or about 93% of the total. Enterprise applications were the largest part of that opportunity. In other words, the IPO story was not primarily that SpaceX could launch more rockets. It was that SpaceX could use its launch advantage, Starlink cash flows, xAI models, X data, compute infrastructure and eventually orbital data centers to compete for one of the largest profit pools in the AI economy.

Simply put, SpaceX presented itself as an N-of-1 company — a business with no clean public-market peer — across three layers. In space, it claimed roughly 650 launches, more than 80% of global mass to orbit since 2023, and more than 95% of 2025 missions flown with one or more reused boosters. In connectivity, it pointed to more than 9,600 Starlink satellites, about 10.3 million subscribers, service in 164 countries and roughly 75% of active maneuverable satellites. In AI, it highlighted more than 1 gigawatt of nameplate compute draw, four major model releases, roughly 350 million daily posts on X, and about 550 million monthly active users across Grok and X.

The roadshow message was therefore straightforward: launch gives SpaceX access to orbit; Starlink gives it a profitable global network; AI gives it the biggest addressable market. The first two make the third more credible.

This is also where Goldman Sachs’ forecast fits into the story. Reuters reported that Goldman expected SpaceX’s AI revenue to rise from $3.2 billion in 2025 to $322 billion by 2030, while total revenue would reach $474 billion. That kind of forecast helps explain why investors were willing to think about SpaceX less like a traditional aerospace company and more like an AI infrastructure platform. But the conflict is obvious: Goldman was also lead underwriter. These projections are useful for understanding the deal narrative, not as a neutral valuation anchor.

That is the central tension. SpaceX came public with real operating proof in launch and Starlink. But the valuation was increasingly justified by AI businesses that are much newer, much more capital-intensive, and much harder to model.

The roadshow message was therefore straightforward: launch gives SpaceX access to orbit; Starlink gives it a profitable global network; AI gives it the biggest addressable market. The first two make the third more credible.

This is also where Goldman Sachs’ forecast fits into the story. Reuters reported that Goldman expected SpaceX’s AI revenue to rise from $3.2 billion in 2025 to $322 billion by 2030, while total revenue would reach $474 billion. That kind of forecast helps explain why investors were willing to think about SpaceX less like a traditional aerospace company and more like an AI infrastructure platform. But the conflict is obvious: Goldman was also lead underwriter. These projections are useful for understanding the deal narrative, not as a neutral valuation anchor.

That is the central tension. SpaceX came public with real operating proof in launch and Starlink. But the valuation was increasingly justified by AI businesses that are much newer, much more capital-intensive, and much harder to model.

4. Demand was not just strong. It was rationed

By the time shares were allocated, the deal had become a scarcity event. Bloomberg reported that the IPO drew more than $350 billion of demand, including more than $250 billion from institutions and more than $100 billion from individual investors. The company reportedly allocated at least 20% of available shares to individuals, while roughly 70% of institutional allocations went to long-only investors and sovereign wealth funds.

On the retail side, a 20% allocation means that most retail demand was left unsatisfied before trading even started. That matters because it created a natural second wave of buying. Investors who wanted shares but received little or no allocation had to buy in the open market. The IPO price discovered institutional demand. The first trading sessions discovered scarcity.

The post-debut data point in the same direction. According to Vanda Research, SpaceX was the most bought stock by retail investors on its first trading day, with net purchases running at more than 3.5 times those of second-place Nvidia. Citadel Securities then reported that June 12 was the largest single day of net buying by individual investors in its dataset. Citadel, which executes roughly 35% of all US-listed retail volume, said retail activity spiked across both equities and options.

This was not just meme-stock speculation. It was broad public demand for a company that had been inaccessible for two decades, arriving at the same time as AI enthusiasm, Musk’s personal following and a tiny initial float.

The IPO did not fully satisfy demand. It rationed it. That made the first days of trading less like a normal valuation exercise and more like a second allocation process, this time in the open market.

On the retail side, a 20% allocation means that most retail demand was left unsatisfied before trading even started. That matters because it created a natural second wave of buying. Investors who wanted shares but received little or no allocation had to buy in the open market. The IPO price discovered institutional demand. The first trading sessions discovered scarcity.

The post-debut data point in the same direction. According to Vanda Research, SpaceX was the most bought stock by retail investors on its first trading day, with net purchases running at more than 3.5 times those of second-place Nvidia. Citadel Securities then reported that June 12 was the largest single day of net buying by individual investors in its dataset. Citadel, which executes roughly 35% of all US-listed retail volume, said retail activity spiked across both equities and options.

This was not just meme-stock speculation. It was broad public demand for a company that had been inaccessible for two decades, arriving at the same time as AI enthusiasm, Musk’s personal following and a tiny initial float.

The IPO did not fully satisfy demand. It rationed it. That made the first days of trading less like a normal valuation exercise and more like a second allocation process, this time in the open market.

5. The first rally was market plumbing, not just enthusiasm

The first rally looked like a simple vote of confidence. It was more complicated than that.

Three forces amplified the opening move.

First, the float was exceptionally small. PitchBook estimated that only 4.2% of SpaceX’s total shares was initially available to trade. In a company valued in the trillions, that created a mismatch between the global investor audience and the number of shares actually available.

Second, the IPO left demand unsatisfied. Some institutions, sovereign wealth funds and retail buyers that received limited allocations still had to build positions in the market. The first-day price was therefore not only a judgment on valuation; it was also a clearing price for scarcity.

There was even a more technical version of this scarcity trade. Bloomberg’s Matt Levine described how some investors appeared to seek “synthetic” exposure to the SpaceX IPO pop through funds that were expected to receive IPO allocations. ARK Innovation ETF, for example, saw a record $4.6 billion inflow shortly before SpaceX began trading and then a $6.2 billion outflow in the following session, while the fund bought roughly 1.7 million SpaceX shares on the listing day. The logic was simple: if investors could not get SpaceX at the IPO price directly, they could try to buy a vehicle that would receive the shares, benefit from the post-listing gain, and then exit. Similar flows appeared around some Baron funds with large SpaceX exposure. This was not the main driver of the stock, but it shows how much effort investors were willing to make to manufacture access to a rationed IPO.

Third, Wall Street’s product machine moved almost immediately. Options and leveraged products turned SpaceX into a tradable volatility instrument from the start. That made the stock accessible not only to long-term investors, but also to retail traders, hedge funds, derivatives desks and short-term momentum players.

The result was a stock that traded not only on fundamentals, but on access, scarcity, unmet demand and leverage.

That explains the first rally. The next question is different: what happens when the initial scarcity premium meets passive buying on one side and insider supply on the other?

Three forces amplified the opening move.

First, the float was exceptionally small. PitchBook estimated that only 4.2% of SpaceX’s total shares was initially available to trade. In a company valued in the trillions, that created a mismatch between the global investor audience and the number of shares actually available.

Second, the IPO left demand unsatisfied. Some institutions, sovereign wealth funds and retail buyers that received limited allocations still had to build positions in the market. The first-day price was therefore not only a judgment on valuation; it was also a clearing price for scarcity.

There was even a more technical version of this scarcity trade. Bloomberg’s Matt Levine described how some investors appeared to seek “synthetic” exposure to the SpaceX IPO pop through funds that were expected to receive IPO allocations. ARK Innovation ETF, for example, saw a record $4.6 billion inflow shortly before SpaceX began trading and then a $6.2 billion outflow in the following session, while the fund bought roughly 1.7 million SpaceX shares on the listing day. The logic was simple: if investors could not get SpaceX at the IPO price directly, they could try to buy a vehicle that would receive the shares, benefit from the post-listing gain, and then exit. Similar flows appeared around some Baron funds with large SpaceX exposure. This was not the main driver of the stock, but it shows how much effort investors were willing to make to manufacture access to a rationed IPO.

Third, Wall Street’s product machine moved almost immediately. Options and leveraged products turned SpaceX into a tradable volatility instrument from the start. That made the stock accessible not only to long-term investors, but also to retail traders, hedge funds, derivatives desks and short-term momentum players.

The result was a stock that traded not only on fundamentals, but on access, scarcity, unmet demand and leverage.

That explains the first rally. The next question is different: what happens when the initial scarcity premium meets passive buying on one side and insider supply on the other?

6. The next test is supply: passive buying versus the lockup staircase

The most important market-structure question is no longer the IPO. It is the supply calendar.

There is a common bull case for giant IPOs: index funds will be forced to buy. That is true, but the timing and size matter. The academic mechanism is real. A Harvard Business School study by Chris Murray and Marco Sammon found that mechanical buying by CRSP-index-tracking funds five days after eligible IPOs caused “Fast Track” IPOs to outperform non-Fast Track peers by more than five percentage points around inclusion, with much of the effect later reverting. It also found that expected index demand affected IPO structure and helped companies raise more capital.

SpaceX looks like a live case study in that mechanism, but with unusual scale. Nasdaq changed its rules so a mega-cap IPO could enter the Nasdaq 100 after only 15 trading days, while FTSE Russell adopted a fast-entry approach closer to five trading days. S&P Dow Jones, by contrast, kept its existing requirements, including seasoning, profitability and public-float rules. That delayed the largest potential passive demand event. Bloomberg Intelligence estimated that fast S&P 500 inclusion could have created roughly $14 billion of forced buying in SpaceX, but that buying will not arrive immediately.

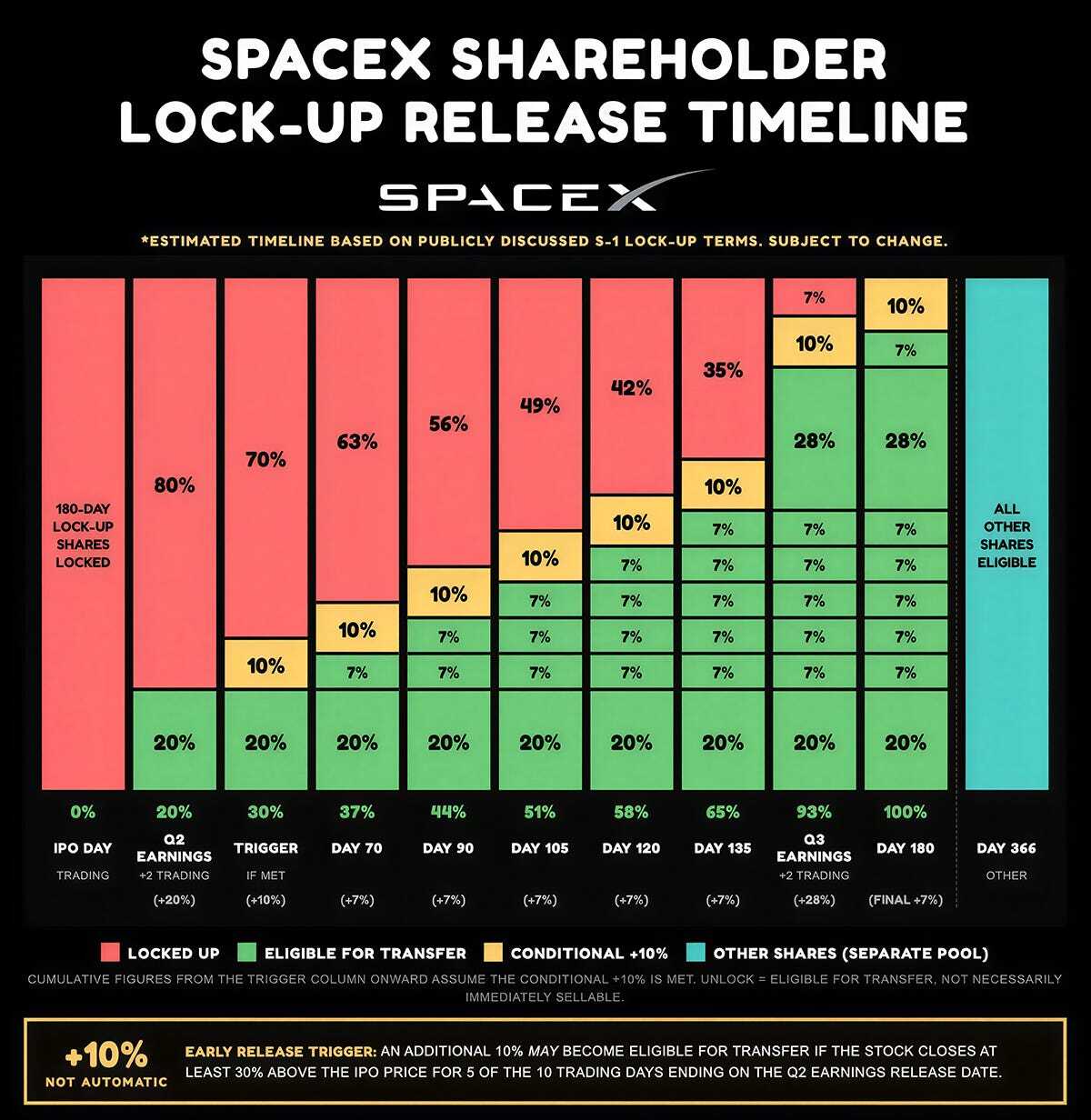

At the same time, the supply calendar is unusually important. SpaceX did not use a simple one-day lockup cliff. It built a staircase. That is smarter than releasing a huge block of insider shares all at once, but a staircase still leads somewhere.

PitchBook estimates that eligible trading supply could rise from about 4% at listing to almost 40% by day 180 and index-related buying could absorb about 8.7% of supply in the first year, which is meaningful but not enough to eliminate the overhang. Musk is different: his shares are subject to a 366-day lockup with no early release provision. The prospectus says shares locked for more than one year include an aggregate of 7.8 billion shares, including 100% of Musk’s shares, representing about 60% of shares outstanding after the offering.

The early release schedule also creates a sequence of market tests. The prospectus describes possible releases after the first earnings release, at day 70, day 90, day 105, day 120, day 135, after Q3 earnings, and at day 180. Each date becomes less about accounting earnings and more about whether fresh demand is strong enough to absorb new supply.

That is why the post-IPO story should be framed less as “will SpaceX beat the next quarter?” and more as “can demand keep absorbing supply at this valuation?”

For the first few weeks, scarcity helped the stock. Over the next year, supply will test it.

There is a common bull case for giant IPOs: index funds will be forced to buy. That is true, but the timing and size matter. The academic mechanism is real. A Harvard Business School study by Chris Murray and Marco Sammon found that mechanical buying by CRSP-index-tracking funds five days after eligible IPOs caused “Fast Track” IPOs to outperform non-Fast Track peers by more than five percentage points around inclusion, with much of the effect later reverting. It also found that expected index demand affected IPO structure and helped companies raise more capital.

SpaceX looks like a live case study in that mechanism, but with unusual scale. Nasdaq changed its rules so a mega-cap IPO could enter the Nasdaq 100 after only 15 trading days, while FTSE Russell adopted a fast-entry approach closer to five trading days. S&P Dow Jones, by contrast, kept its existing requirements, including seasoning, profitability and public-float rules. That delayed the largest potential passive demand event. Bloomberg Intelligence estimated that fast S&P 500 inclusion could have created roughly $14 billion of forced buying in SpaceX, but that buying will not arrive immediately.

At the same time, the supply calendar is unusually important. SpaceX did not use a simple one-day lockup cliff. It built a staircase. That is smarter than releasing a huge block of insider shares all at once, but a staircase still leads somewhere.

PitchBook estimates that eligible trading supply could rise from about 4% at listing to almost 40% by day 180 and index-related buying could absorb about 8.7% of supply in the first year, which is meaningful but not enough to eliminate the overhang. Musk is different: his shares are subject to a 366-day lockup with no early release provision. The prospectus says shares locked for more than one year include an aggregate of 7.8 billion shares, including 100% of Musk’s shares, representing about 60% of shares outstanding after the offering.

The early release schedule also creates a sequence of market tests. The prospectus describes possible releases after the first earnings release, at day 70, day 90, day 105, day 120, day 135, after Q3 earnings, and at day 180. Each date becomes less about accounting earnings and more about whether fresh demand is strong enough to absorb new supply.

That is why the post-IPO story should be framed less as “will SpaceX beat the next quarter?” and more as “can demand keep absorbing supply at this valuation?”

For the first few weeks, scarcity helped the stock. Over the next year, supply will test it.

7. Once scarcity fades, valuation becomes the debate

The valuation debate is not about whether SpaceX is an extraordinary company. It is. The debate is about how much of that extraordinary future was already paid for in the IPO price.

There are three useful ways to frame that debate: a conservative fair-value view, a story-driven founder/AI view, and a market-multiple view. They disagree on fair value, but they agree on one thing: the current price depends heavily on future AI success.

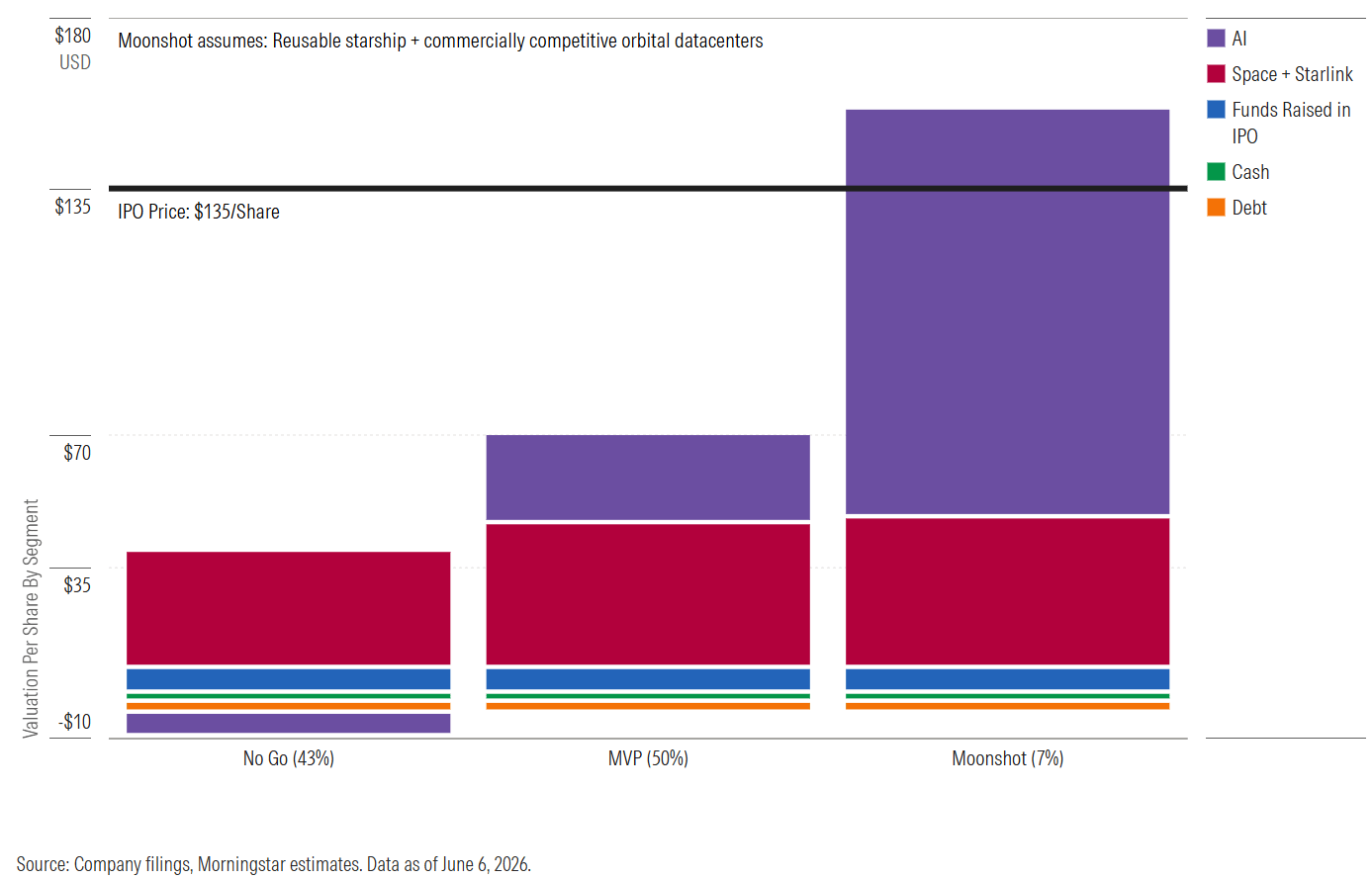

The first is Morningstar’s. Morningstar values SpaceX at about $63 per share, far below the $135 IPO price. Its point is not that SpaceX lacks value. The core launch and Starlink businesses are real strategic assets, and Morningstar assigns the company a narrow moat based on launch cost advantages, scale and satellite communications. But in its framework, the IPO price requires too much confidence in unproven technologies: rapid Starship reusability, commercially viable orbital AI data centers, and very large-scale AI monetization.

Morningstar’s scenario work makes this clear. It estimates that the core space and connectivity businesses contribute about $40 per share to fair value. The rest of the IPO valuation depends heavily on AI optionality and future moonshots. In its most optimistic “Moonshot” scenario, SpaceX successfully develops rapidly reusable Starship and commercially competitive orbital data centers, and the stock can approach or exceed the IPO price. But Morningstar assigns that scenario only a 7% probability. To justify the $135 offering price, investors would need to treat that Moonshot outcome as far more likely.

There are three useful ways to frame that debate: a conservative fair-value view, a story-driven founder/AI view, and a market-multiple view. They disagree on fair value, but they agree on one thing: the current price depends heavily on future AI success.

The first is Morningstar’s. Morningstar values SpaceX at about $63 per share, far below the $135 IPO price. Its point is not that SpaceX lacks value. The core launch and Starlink businesses are real strategic assets, and Morningstar assigns the company a narrow moat based on launch cost advantages, scale and satellite communications. But in its framework, the IPO price requires too much confidence in unproven technologies: rapid Starship reusability, commercially viable orbital AI data centers, and very large-scale AI monetization.

Morningstar’s scenario work makes this clear. It estimates that the core space and connectivity businesses contribute about $40 per share to fair value. The rest of the IPO valuation depends heavily on AI optionality and future moonshots. In its most optimistic “Moonshot” scenario, SpaceX successfully develops rapidly reusable Starship and commercially competitive orbital data centers, and the stock can approach or exceed the IPO price. But Morningstar assigns that scenario only a 7% probability. To justify the $135 offering price, investors would need to treat that Moonshot outcome as far more likely.

The second is Aswath Damodaran’s, which is useful because it separates story from numbers. Before the prospectus, Damodaran valued SpaceX at roughly $1.2 trillion using limited public information. After the filing, he updated the model with actual financials. The prospectus confirmed that his launch and Starlink revenue assumptions were broadly close, but xAI revenue was higher than he expected, the operating loss was larger, interest expense was close to $2 billion, and the company reported a net loss of about $5 billion. He also noted that xAI changed the balance sheet: book equity rose to about $41.3 billion, total debt including leases rose to $22.9 billion, and cash stood at $24.7 billion, leaving net debt slightly negative. In his model, existing debt was therefore not the main valuation issue because it was small relative to an enterprise value above $1 trillion.

The more important point from Damodaran is qualitative. SpaceX is not a clean aerospace valuation anymore. It is a “loaded bet on AI and Elon Musk.” His post-prospectus equity value was around $1.3 trillion, or roughly $100 per share after adding expected IPO proceeds. That sits below the $135 IPO price but well above Morningstar’s fair value, which makes it a useful middle ground: not dismissive, but not willing to fully pay for the IPO story either.

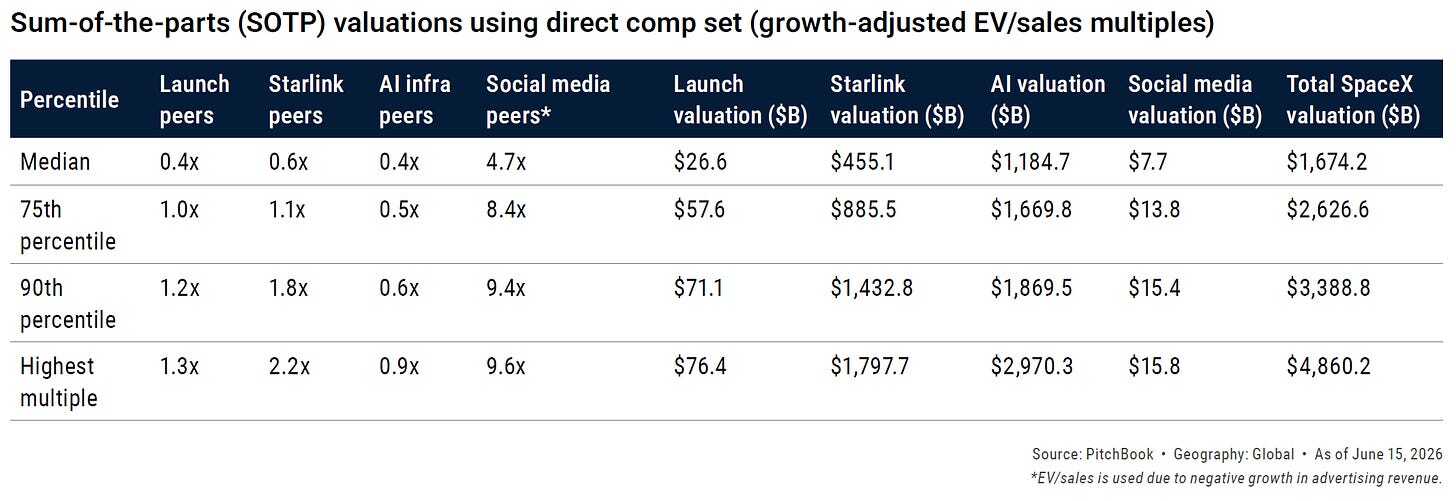

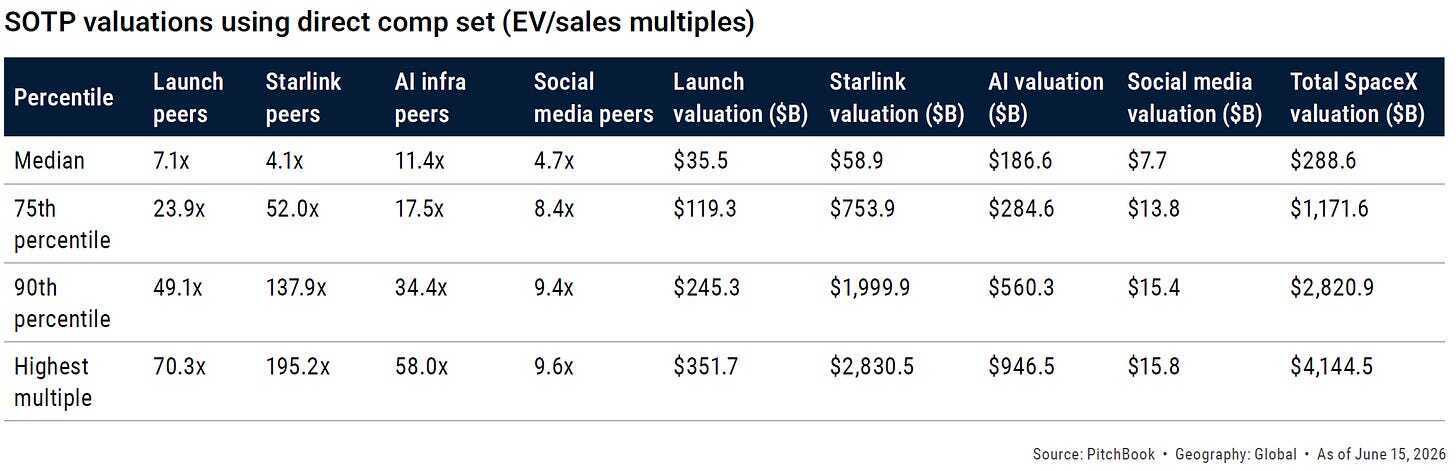

The third is PitchBook’s, and it is probably the most useful for understanding where the stock actually traded. PitchBook values SpaceX’s launch-plus-connectivity core at roughly $1.5 trillion, placing it at the 90th percentile of its growth-adjusted peer set. That is a generous treatment, but it is not unreasonable: connectivity generated 61% of 2025 revenue, virtually all of free cash flow, and a 63% segment-adjusted EBITDA margin, which exceeds every telecom and satellite peer PitchBook tracks and approaches enterprise software margins.

The gap between that $1.5 trillion core and the roughly $2.5 trillion enterprise value after the early rally is the AI premium. PitchBook estimates that applying median AI-infrastructure multiples to SpaceX’s AI segment bridges the valuation to about $2.7 trillion, close to where the stock traded after the first surge. Its growth-adjusted SOTP table values SpaceX at about $1.67 trillion at the median, $2.63 trillion at the 75th percentile, $3.39 trillion at the 90th percentile, and $4.86 trillion at the highest peer multiple.

The more important point from Damodaran is qualitative. SpaceX is not a clean aerospace valuation anymore. It is a “loaded bet on AI and Elon Musk.” His post-prospectus equity value was around $1.3 trillion, or roughly $100 per share after adding expected IPO proceeds. That sits below the $135 IPO price but well above Morningstar’s fair value, which makes it a useful middle ground: not dismissive, but not willing to fully pay for the IPO story either.

The third is PitchBook’s, and it is probably the most useful for understanding where the stock actually traded. PitchBook values SpaceX’s launch-plus-connectivity core at roughly $1.5 trillion, placing it at the 90th percentile of its growth-adjusted peer set. That is a generous treatment, but it is not unreasonable: connectivity generated 61% of 2025 revenue, virtually all of free cash flow, and a 63% segment-adjusted EBITDA margin, which exceeds every telecom and satellite peer PitchBook tracks and approaches enterprise software margins.

The gap between that $1.5 trillion core and the roughly $2.5 trillion enterprise value after the early rally is the AI premium. PitchBook estimates that applying median AI-infrastructure multiples to SpaceX’s AI segment bridges the valuation to about $2.7 trillion, close to where the stock traded after the first surge. Its growth-adjusted SOTP table values SpaceX at about $1.67 trillion at the median, $2.63 trillion at the 75th percentile, $3.39 trillion at the 90th percentile, and $4.86 trillion at the highest peer multiple.

But PitchBook also shows the downside if growth is not capitalized so generously. On flat EV/sales multiples against 2026 estimates — essentially stripping out the growth premium — its SOTP produces only $289 billion at the median, $1.17 trillion at the 75th percentile, and reaches the current price only near the 90th percentile. That is the whole risk in one chart: the market is not valuing SpaceX as a current cash-flow asset. It is valuing it as a growth platform.

PitchBook’s conclusion is balanced. The AI premium is not vapor. It is backed by real contracted revenue. Anthropic and Google compute deals reportedly run at about $26 billion annualized, using roughly 73% of current Colossus I and II capacity and half of planned capacity. If SpaceX leased its full planned 1.5-gigawatt buildout, the run-rate could approach $60 billion. But those contracts are fragile: they are terminable on 90 days’ notice, and the durable moat in AI infrastructure depends on compute capacity remaining scarce. If capacity becomes abundant, or if counterparties build their own infrastructure, the premium becomes harder to defend.

That is the cleanest way to state the valuation question: SpaceX has a defensible launch-and-Starlink core plus a very large AI call option. The stock price tells us the market is already paying heavily for both.

That is the cleanest way to state the valuation question: SpaceX has a defensible launch-and-Starlink core plus a very large AI call option. The stock price tells us the market is already paying heavily for both.

8. Starlink is the core. AI is the option. Starship is the unlock

The simplest way to understand SpaceX is this:

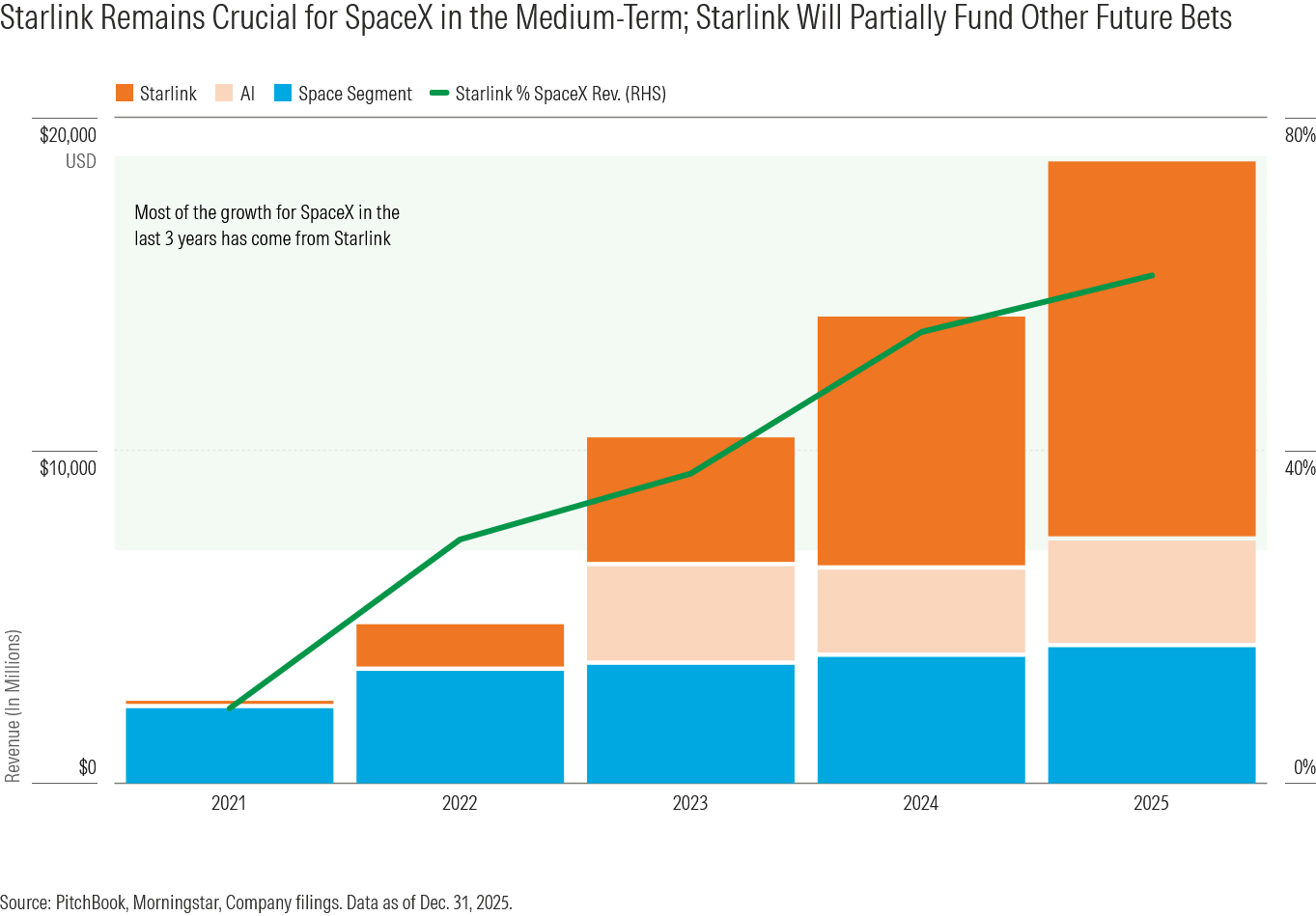

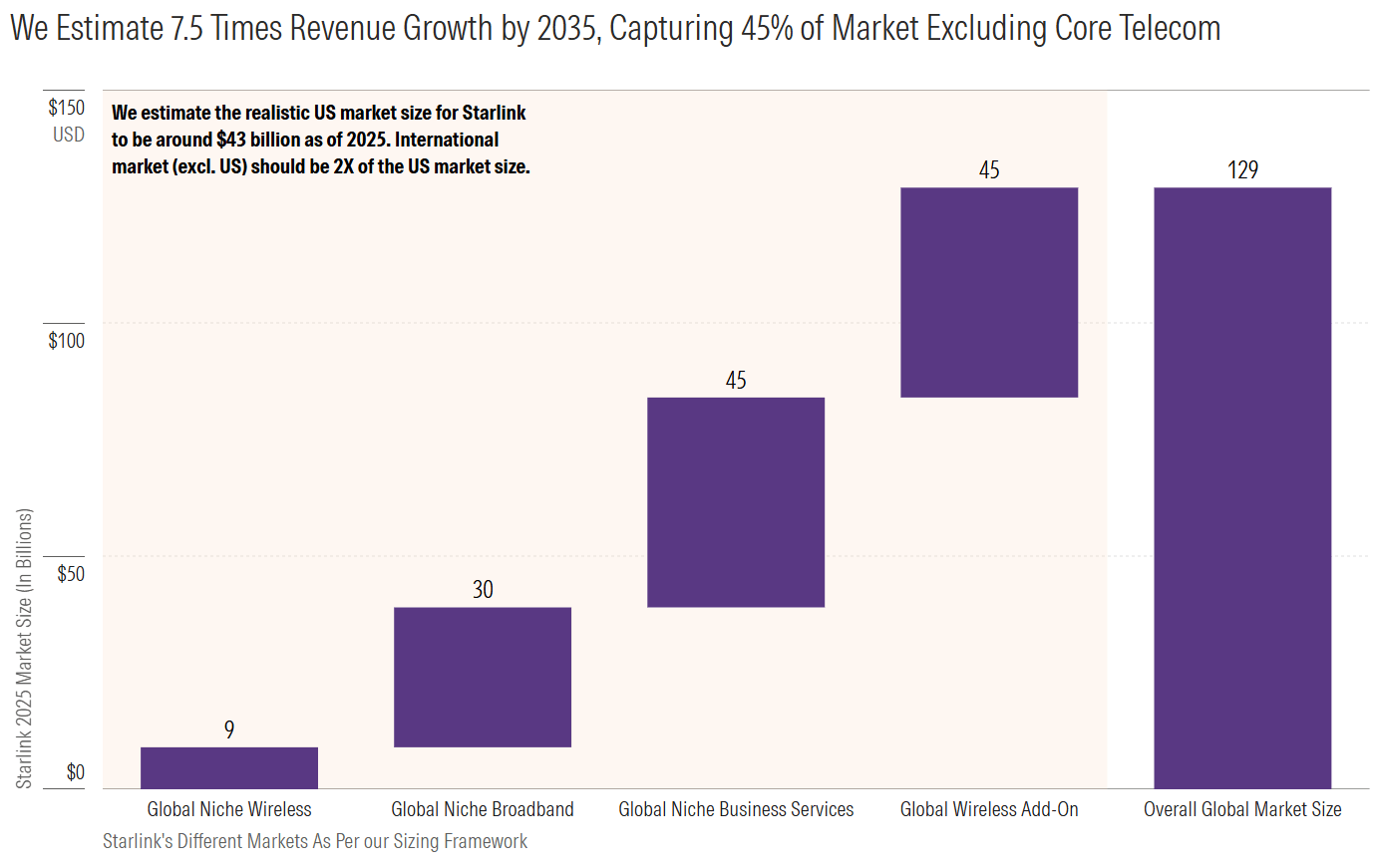

Starlink is the current cash machine. Morningstar’s Starlink market-sizing work argues that Starlink will remain SpaceX’s main moneymaker in the medium term, though it is skeptical of SpaceX’s much larger stated TAM. Morningstar estimates a realistic Starlink global opportunity of about $129 billion as of 2025, with Starlink penetrating about 45% of that opportunity by 2035 in its base-case forecast.

Starlink is the current cash machine. Morningstar’s Starlink market-sizing work argues that Starlink will remain SpaceX’s main moneymaker in the medium term, though it is skeptical of SpaceX’s much larger stated TAM. Morningstar estimates a realistic Starlink global opportunity of about $129 billion as of 2025, with Starlink penetrating about 45% of that opportunity by 2035 in its base-case forecast.

AI is the valuation accelerant. The Goldman forecast discussed earlier — AI revenue rising from $3.2 billion in 2025 to $322 billion by 2030 — explains why investors were willing to apply hyperscaler-like valuation logic to what used to be viewed primarily as a rocket-and-satellite company. But it also shows how much of the bull case rests on an AI ramp that has barely begun.

Starship is the operational unlock. It lowers the cost of deploying more Starlink capacity, enables larger satellites, makes orbital infrastructure more plausible, and supports the company’s deeper-space ambitions. The prospectus says SpaceX spent about $3.0 billion of Space segment R&D on Starship in 2025, which is why the Space segment can be strategically dominant while still reporting an operating loss.

That triad — Starlink cash, AI optionality, Starship unlock — is the real bull case.

Starship is the operational unlock. It lowers the cost of deploying more Starlink capacity, enables larger satellites, makes orbital infrastructure more plausible, and supports the company’s deeper-space ambitions. The prospectus says SpaceX spent about $3.0 billion of Space segment R&D on Starship in 2025, which is why the Space segment can be strategically dominant while still reporting an operating loss.

That triad — Starlink cash, AI optionality, Starship unlock — is the real bull case.

9. But the public market will not grade SpaceX on vision alone

SpaceX now has to live on a public-market calendar. That is new.

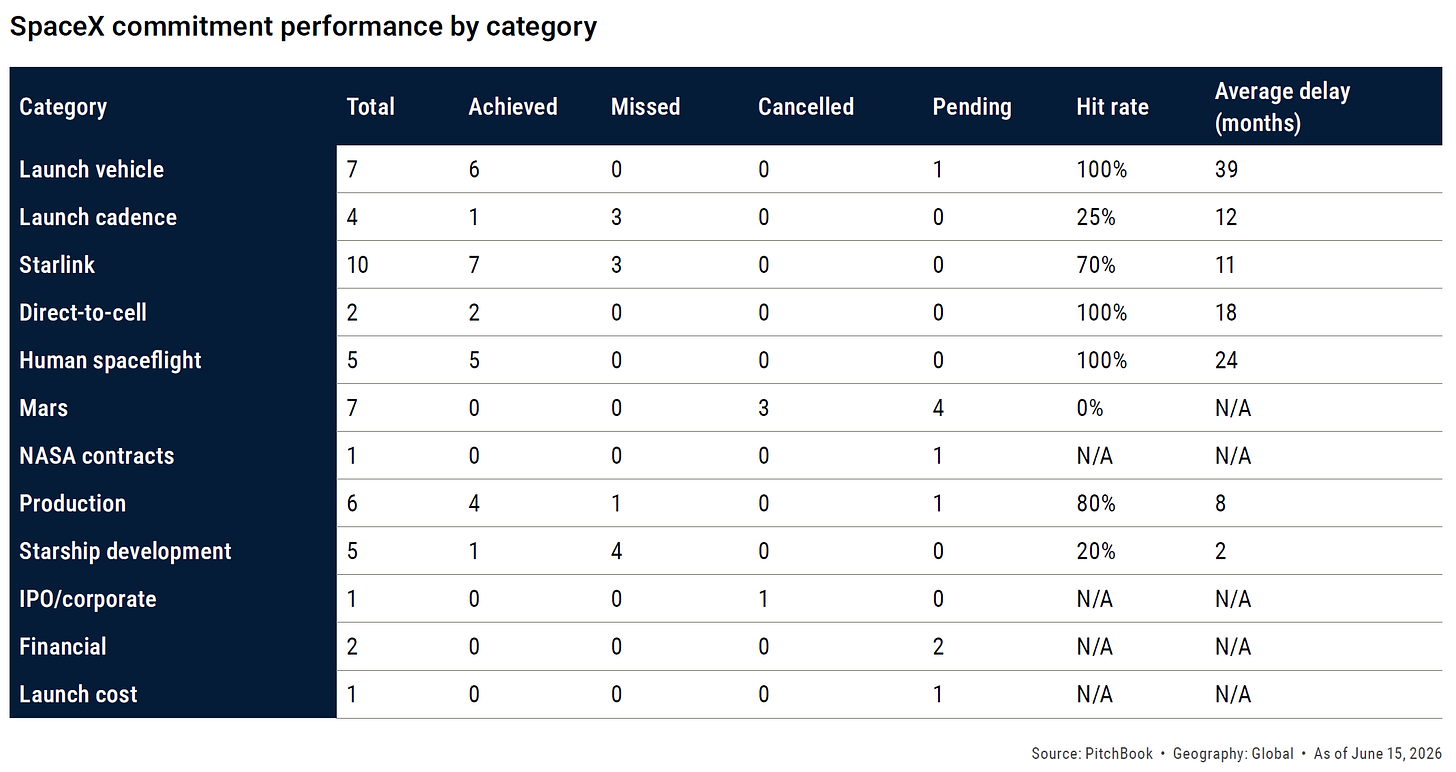

PitchBook’s “credibility ledger” is useful here. It reviewed 51 SpaceX commitments and found that the company eventually delivered 66% of those with definitive outcomes, but only 17% on time, with an average delay of about 19.7 months. Its conclusion is not that SpaceX fails. It is that SpaceX tends to do what it says, but rarely when it says.

That distinction matters for a stock trading at a valuation that embeds ambitious timelines. PitchBook recommends applying roughly a two-year discount to stated SpaceX timelines, especially for frontier goals like Starship cadence, orbital refueling and Mars.

The near-term watchlist is clear: first commercial Starship payload delivery, V3 Starlink satellite launches, Starlink Mobile subscriber progress, the first few earnings reports, AI compute contract durability, and FAA/FCC regulatory milestones.

PitchBook’s “credibility ledger” is useful here. It reviewed 51 SpaceX commitments and found that the company eventually delivered 66% of those with definitive outcomes, but only 17% on time, with an average delay of about 19.7 months. Its conclusion is not that SpaceX fails. It is that SpaceX tends to do what it says, but rarely when it says.

That distinction matters for a stock trading at a valuation that embeds ambitious timelines. PitchBook recommends applying roughly a two-year discount to stated SpaceX timelines, especially for frontier goals like Starship cadence, orbital refueling and Mars.

The near-term watchlist is clear: first commercial Starship payload delivery, V3 Starlink satellite launches, Starlink Mobile subscriber progress, the first few earnings reports, AI compute contract durability, and FAA/FCC regulatory milestones.

10. The hidden cost of the AI pivot: debt and capex

The bond sale should not be treated as the single reason for the first selloff. Low-float IPOs can reverse for many reasons. But debt and capex matter for the longer-term investment case because SpaceX’s AI ambitions require enormous capital before the full revenue opportunity is proven.

The prospectus already showed how the xAI/X combination changed the balance sheet. In March 2026, SpaceX entered into a $20 billion bridge loan, maturing in September 2027 with possible extensions into March 2028. The proceeds were used to repay X and xAI-related obligations, and the refinancing included a $1.163 billion prepayment penalty. Bloomberg later reported that SpaceX raised $25 billion in its debut investment-grade bond sale after the IPO, with proceeds expected to refinance the bridge loan and fund general corporate needs. The bond plan followed ratings in the BBB tier from Moody’s, S&P and Fitch. Demand was solid but not euphoric: the final order book was reportedly less than three times the amount of debt offered, below the recent high-grade market average, and the 2036 bonds priced at a wider spread than similarly rated BBB debt. That is a useful contrast with the equity IPO. Stock investors were buying upside; bondholders were asking to be paid for execution risk.

This is unusual. SpaceX is not coming to credit markets like a mature industrial borrower with stable free cash flow and modest capital needs. It is coming as a dominant launch company and profitable Starlink operator that has also bolted on a deeply capital-intensive AI business.

The numbers show the scale of the shift. Bloomberg reported that SpaceX had $29.1 billion of long-term debt as of March 31, with the bridge loan making up the bulk of it. Rating-agency and Wall Street forecasts point to much heavier funding needs ahead. S&P expects SpaceX to remain cash-flow negative until 2030, with burn rising sharply next year and again in 2028. It also expects borrowings to climb to about $132 billion in 2028, up from close to zero on a net basis after adjusting for cash and lease liabilities.

The capex path is even more striking. Goldman Sachs and Evercore ISI reportedly expect SpaceX capital expenditures to rise to more than $360 billion in 2030, up from more than $20 billion last year. Goldman’s team penciled in a free-cash-flow trough of negative $105 billion in 2029 before a recovery to more than $72 billion positive free cash flow in 2031.

Those forecasts are not neutral facts; they come from banks and research teams trying to model a very unusual company. But they are still useful because they show what the AI story requires. Training clusters, power infrastructure, data centers, chip supply, cooling systems, batteries and future orbital compute are not low-capex software businesses. They are industrial projects. Terafab is the clearest example. SpaceX describes it as a planned chip-manufacturing initiative with Tesla and Intel that would bring more of the AI hardware stack in-house, with the long-term goal of producing one terawatt of compute hardware annually. The strategic logic is obvious: if AI compute is constrained by chips, power and data-center infrastructure, SpaceX wants control over more of that physical stack. But it is still early. The prospectus says specific Terafab projects, timelines, milestones and capital expenditures have not yet been determined.

The company does have real contracted revenue to support the story. Bloomberg reported a $30 billion cloud-services deal with Google running through mid-2029 and a roughly $45 billion Anthropic deal over about three years. These are the same contracts that help support the AI premium discussed above. But they also highlight the circular risk: the AI premium rests partly on contracts that justify capex, while the capex is needed to prove the AI premium.

For equity investors, the key question is not whether SpaceX can raise capital. After the IPO and bond-market access, it clearly can. The question is whether that capital will earn returns high enough to justify the valuation already placed on the stock.

Starlink may generate cash. Launch may provide strategic dominance. But AI can consume cash faster than almost any business in history. That is the hidden cost of turning SpaceX from a space-and-connectivity company into an AI infrastructure bet.

The prospectus already showed how the xAI/X combination changed the balance sheet. In March 2026, SpaceX entered into a $20 billion bridge loan, maturing in September 2027 with possible extensions into March 2028. The proceeds were used to repay X and xAI-related obligations, and the refinancing included a $1.163 billion prepayment penalty. Bloomberg later reported that SpaceX raised $25 billion in its debut investment-grade bond sale after the IPO, with proceeds expected to refinance the bridge loan and fund general corporate needs. The bond plan followed ratings in the BBB tier from Moody’s, S&P and Fitch. Demand was solid but not euphoric: the final order book was reportedly less than three times the amount of debt offered, below the recent high-grade market average, and the 2036 bonds priced at a wider spread than similarly rated BBB debt. That is a useful contrast with the equity IPO. Stock investors were buying upside; bondholders were asking to be paid for execution risk.

This is unusual. SpaceX is not coming to credit markets like a mature industrial borrower with stable free cash flow and modest capital needs. It is coming as a dominant launch company and profitable Starlink operator that has also bolted on a deeply capital-intensive AI business.

The numbers show the scale of the shift. Bloomberg reported that SpaceX had $29.1 billion of long-term debt as of March 31, with the bridge loan making up the bulk of it. Rating-agency and Wall Street forecasts point to much heavier funding needs ahead. S&P expects SpaceX to remain cash-flow negative until 2030, with burn rising sharply next year and again in 2028. It also expects borrowings to climb to about $132 billion in 2028, up from close to zero on a net basis after adjusting for cash and lease liabilities.

The capex path is even more striking. Goldman Sachs and Evercore ISI reportedly expect SpaceX capital expenditures to rise to more than $360 billion in 2030, up from more than $20 billion last year. Goldman’s team penciled in a free-cash-flow trough of negative $105 billion in 2029 before a recovery to more than $72 billion positive free cash flow in 2031.

Those forecasts are not neutral facts; they come from banks and research teams trying to model a very unusual company. But they are still useful because they show what the AI story requires. Training clusters, power infrastructure, data centers, chip supply, cooling systems, batteries and future orbital compute are not low-capex software businesses. They are industrial projects. Terafab is the clearest example. SpaceX describes it as a planned chip-manufacturing initiative with Tesla and Intel that would bring more of the AI hardware stack in-house, with the long-term goal of producing one terawatt of compute hardware annually. The strategic logic is obvious: if AI compute is constrained by chips, power and data-center infrastructure, SpaceX wants control over more of that physical stack. But it is still early. The prospectus says specific Terafab projects, timelines, milestones and capital expenditures have not yet been determined.

The company does have real contracted revenue to support the story. Bloomberg reported a $30 billion cloud-services deal with Google running through mid-2029 and a roughly $45 billion Anthropic deal over about three years. These are the same contracts that help support the AI premium discussed above. But they also highlight the circular risk: the AI premium rests partly on contracts that justify capex, while the capex is needed to prove the AI premium.

For equity investors, the key question is not whether SpaceX can raise capital. After the IPO and bond-market access, it clearly can. The question is whether that capital will earn returns high enough to justify the valuation already placed on the stock.

Starlink may generate cash. Launch may provide strategic dominance. But AI can consume cash faster than almost any business in history. That is the hidden cost of turning SpaceX from a space-and-connectivity company into an AI infrastructure bet.

11. The investment thesis

SpaceX is not a normal IPO. It is a real industrial achievement, a satellite internet business, an AI infrastructure bet, a Musk premium, a retail-access event and an index-flow problem wrapped into one ticker.

That is why the first two weeks were so violent. Investors were not only deciding what SpaceX is worth. They were deciding what kind of company it is.

Is it a launch monopoly with a profitable satellite network? Is it an AI infrastructure challenger? Is it the next Tesla-style story stock? Is it a public-market gateway into Elon Musk’s most ambitious projects? The answer may be yes to all of them.

Governance is part of that package. Public investors are buying economic exposure, not control. Musk still controls roughly 85% of the voting power through Class B shares, giving him practical control over the board, strategy, capital allocation and major corporate decisions. That control is one reason the stock carries a premium: investors are partly paying for Musk’s ability to push through technically ambitious projects that few conventional management teams would attempt. But it is also a discount that may matter more in periods of stress: related-party transactions, large capital commitments, conflicts with Tesla, X or xAI, or mission-driven decisions that prioritize long-term ambition over minority shareholders.

The danger is that each layer can justify paying a little more. Starlink deserves a premium. Launch dominance deserves a premium. AI optionality deserves a premium. Musk gets a premium. Scarcity gets a premium. Index inclusion gets a premium. But when every layer receives a premium at the same time, the margin for disappointment becomes thin.

SpaceX may become one of the defining companies of the next technological era. The harder question is whether public investors already paid for too much of that future in the first weeks of trading.

That is why the first two weeks were so violent. Investors were not only deciding what SpaceX is worth. They were deciding what kind of company it is.

Is it a launch monopoly with a profitable satellite network? Is it an AI infrastructure challenger? Is it the next Tesla-style story stock? Is it a public-market gateway into Elon Musk’s most ambitious projects? The answer may be yes to all of them.

Governance is part of that package. Public investors are buying economic exposure, not control. Musk still controls roughly 85% of the voting power through Class B shares, giving him practical control over the board, strategy, capital allocation and major corporate decisions. That control is one reason the stock carries a premium: investors are partly paying for Musk’s ability to push through technically ambitious projects that few conventional management teams would attempt. But it is also a discount that may matter more in periods of stress: related-party transactions, large capital commitments, conflicts with Tesla, X or xAI, or mission-driven decisions that prioritize long-term ambition over minority shareholders.

The danger is that each layer can justify paying a little more. Starlink deserves a premium. Launch dominance deserves a premium. AI optionality deserves a premium. Musk gets a premium. Scarcity gets a premium. Index inclusion gets a premium. But when every layer receives a premium at the same time, the margin for disappointment becomes thin.

SpaceX may become one of the defining companies of the next technological era. The harder question is whether public investors already paid for too much of that future in the first weeks of trading.

June April 2026 Bank of America Global Fund Manager Survey

The June Bank of America Global Fund Manager Survey shows investors taking some risk off the table after May’s aggressive chase into equities, but not abandoning the view that growth and earnings can keep improving. BofA’s broad sentiment measure eased to 6.0 from 6.6, still consistent with constructive positioning rather than a broad retreat from risk,

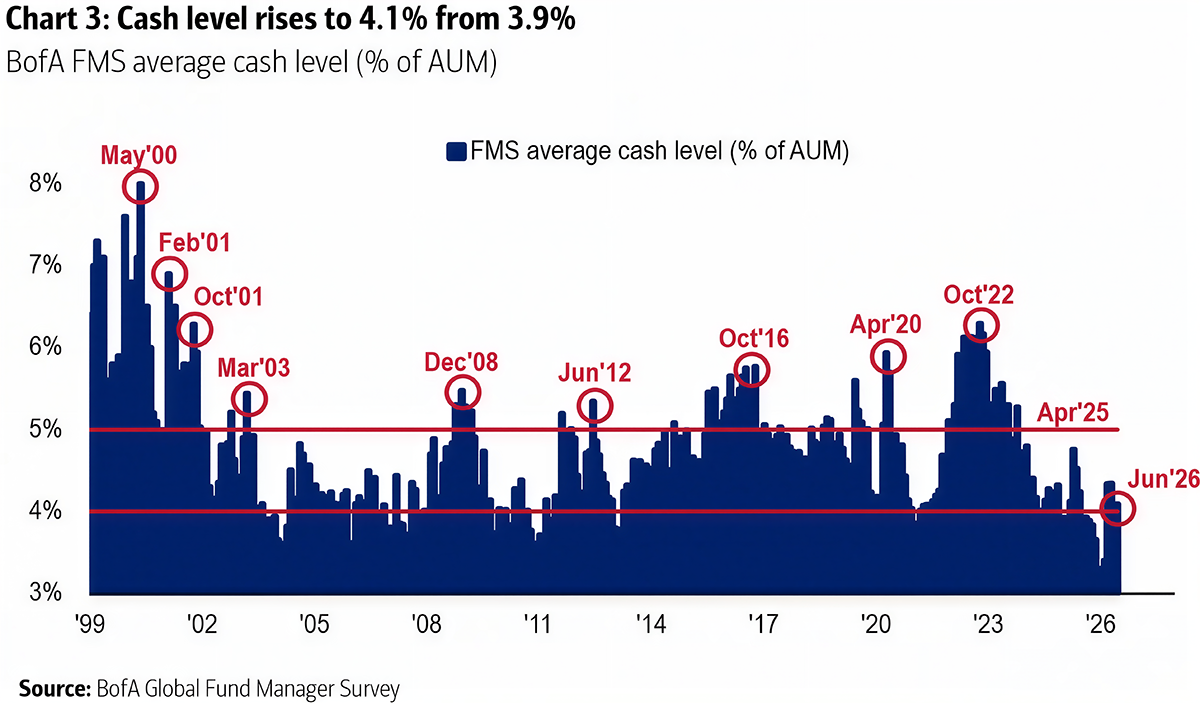

while cash rose only modestly to 4.1% from 3.9%, remaining historically low.

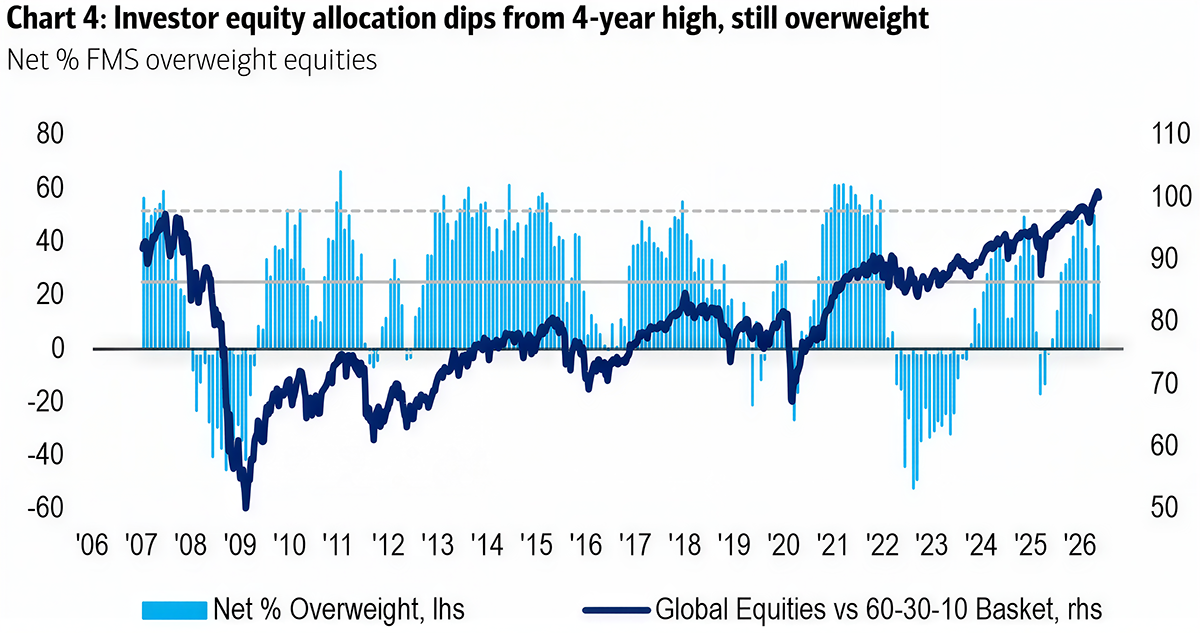

Equity allocation declined to a net 38% overweight from 50%, but remains elevated after May’s four-year high,

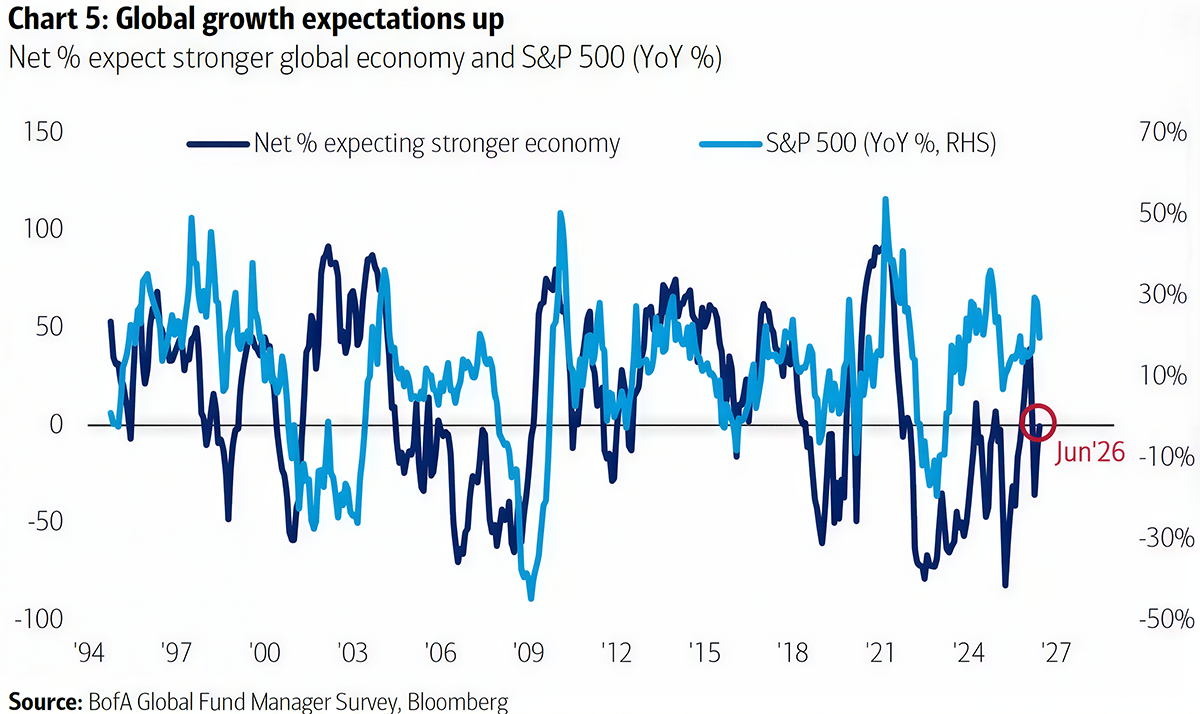

while global growth expectations improved further to net -1% from -14%, and profit expectations reached a three-month high. This combination suggests investors are not calling a market top; rather, they appear to be taking “summer chips” off the table after a powerful rally while keeping a broadly pro-risk stance.

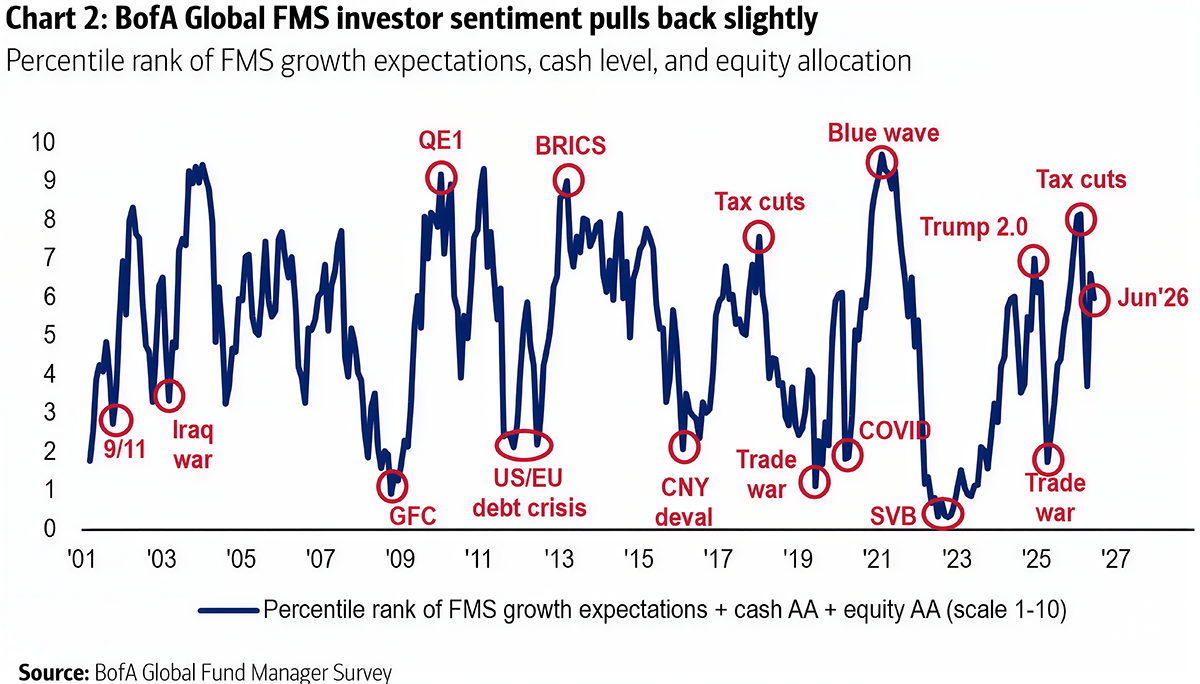

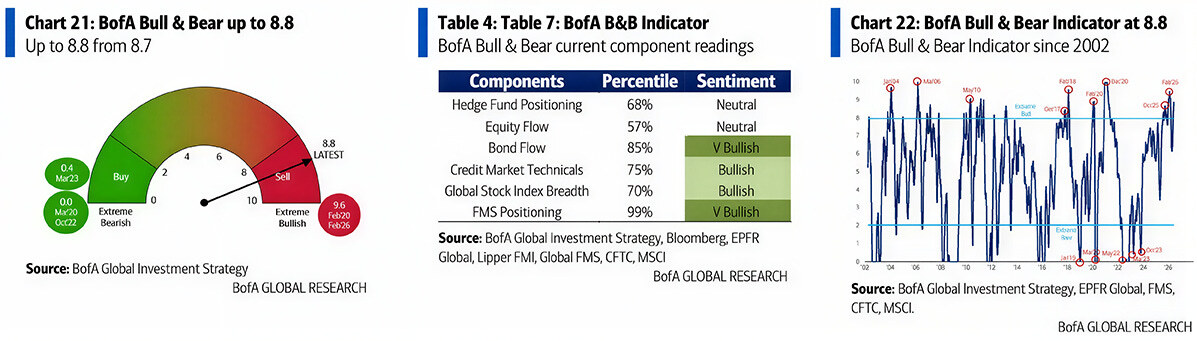

At the same time, positioning warnings are no longer absent. In Michael Hartnett’s June 12 Flow Show, BofA’s Bull & Bear Indicator rose to 8.8 from 8.7, moving further into the “sell” zone. The signal appears to be driven mainly by very bullish FMS positioning, strong bond flows and constructive credit-market technicals, while hedge-fund positioning and equity flows remain more neutral. This does not necessarily mean a major market top is already in place, but it does suggest that positioning has become optimistic enough to leave markets more exposed to profit-taking if yields, inflation or earnings disappoint.

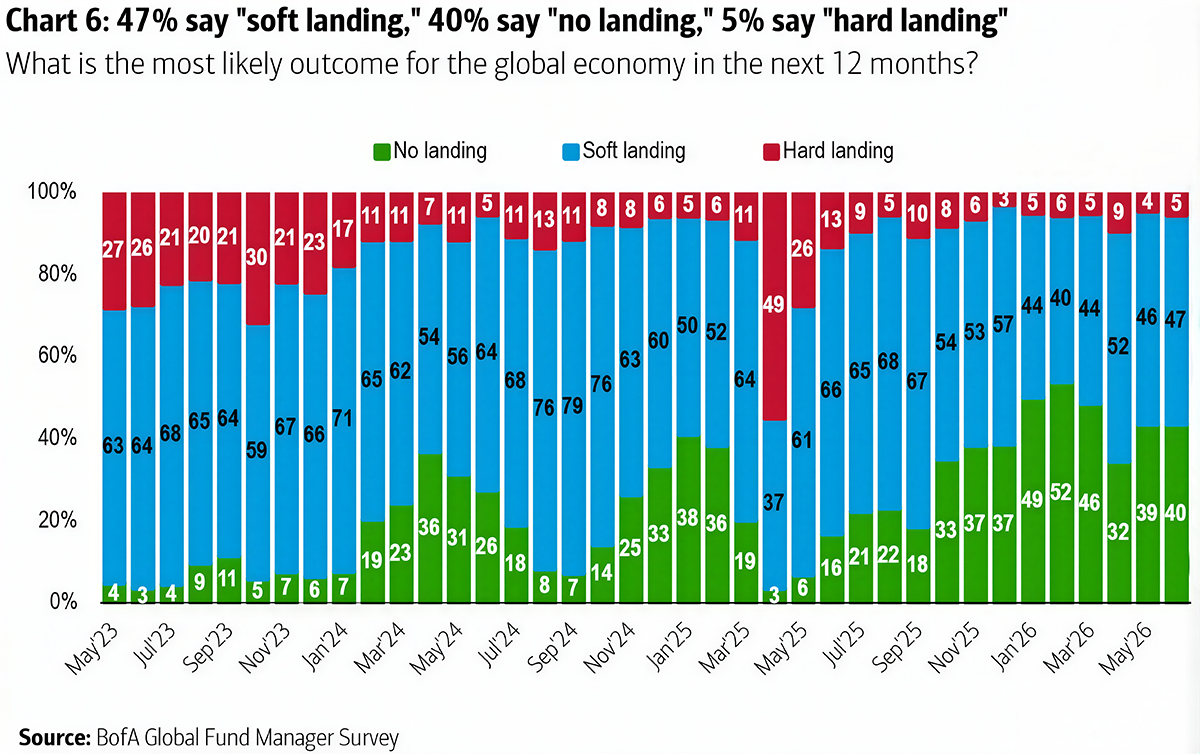

The macro picture has become less pessimistic but more complicated by rates. Only 5% of investors now expect a hard landing, while 47% see a soft landing and 40% expect no landing, leaving recession fears low.

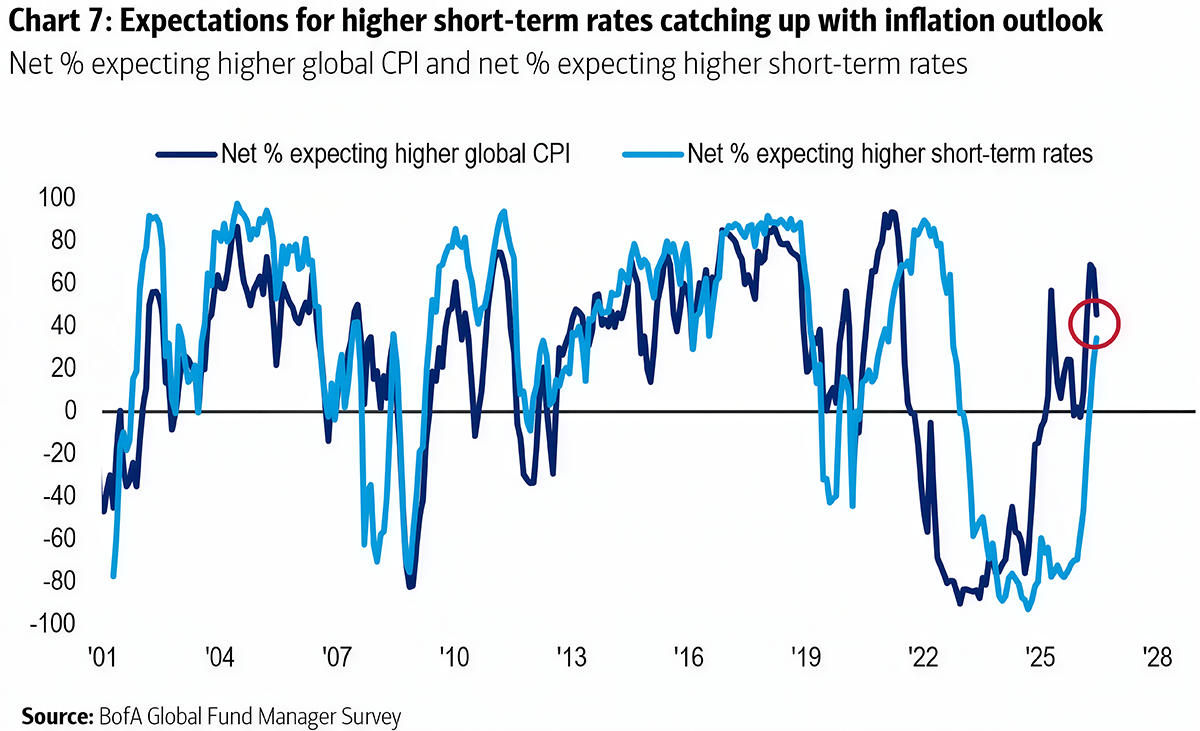

Inflation worries have cooled from May, with the share expecting higher global CPI falling to net 45%, but rate expectations have moved the other way: a net 34% now expect higher short-term rates, the highest since September 2022.

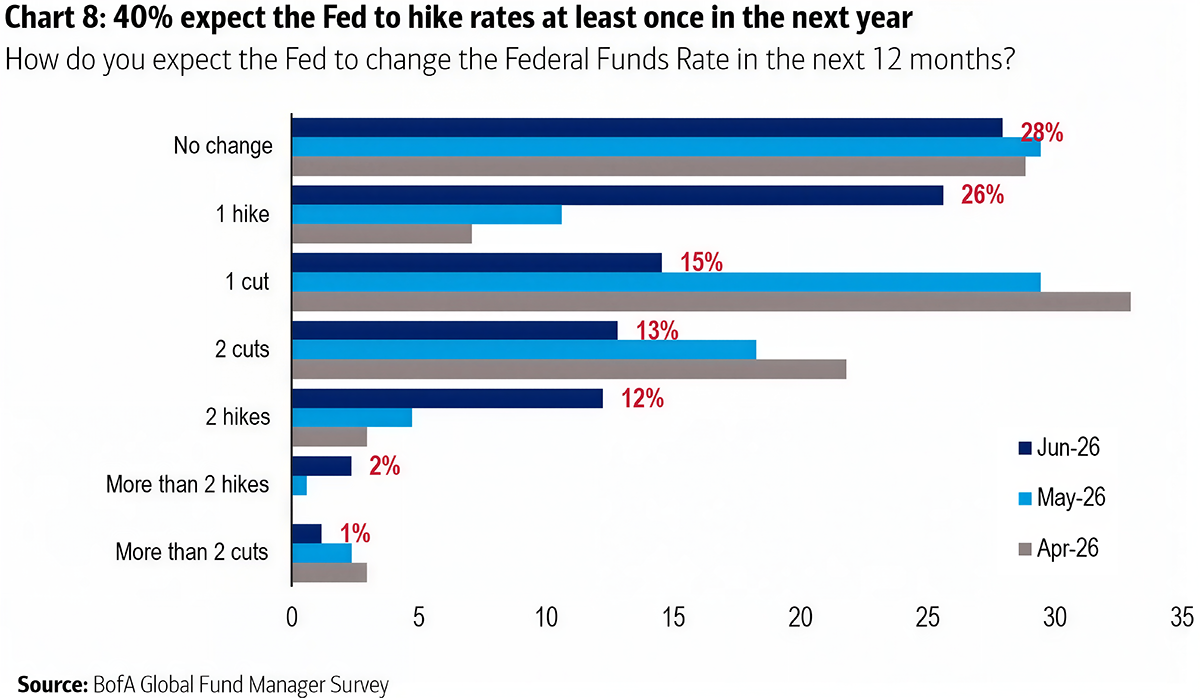

Fed expectations have also shifted sharply hawkish, with 40% now expecting at least one rate hike over the next 12 months versus 16% in May. Only 29% expect one cut and 13% expect two cuts, while 28% expect no change. This is a major change from the earlier “Fed cuts support equities” narrative and suggests the market is increasingly vulnerable to bond-yield pressure if inflation proves sticky.

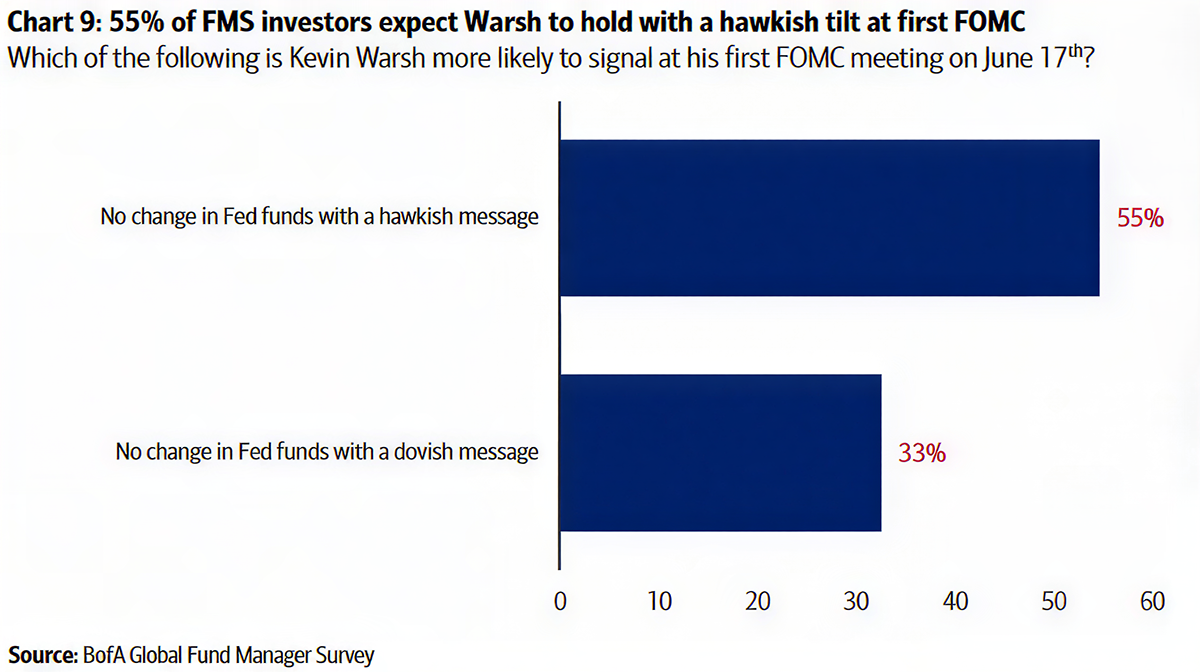

Investors also expect a hawkish policy message at the next FOMC, with 55% expecting no change in the Fed funds rate but a hawkish tone, versus 33% expecting a dovish hold.

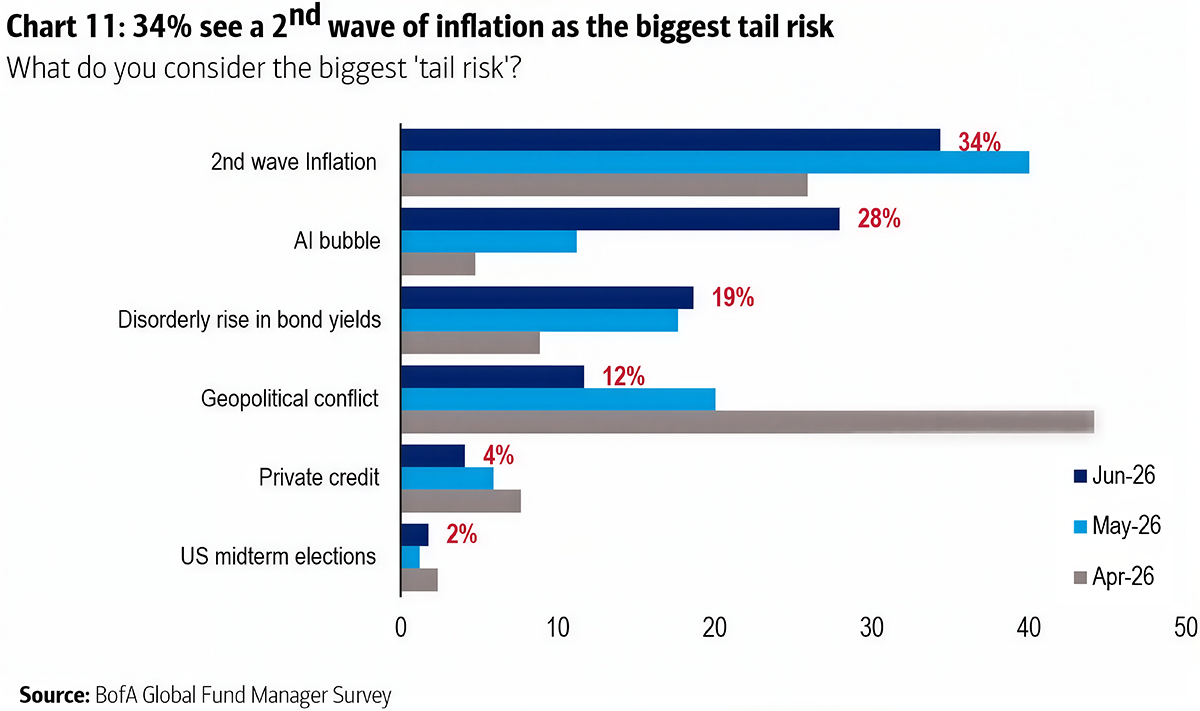

Risk perception has rotated from geopolitics back toward inflation and AI. “Second wave inflation” remains the top tail risk at 34%, followed by “AI bubble” at 28%, while geopolitical conflict has fallen sharply to 12% from 44% two months earlier. This matters because the market’s main risk is no longer only an external shock, but the interaction between sticky inflation, higher rates and crowded technology positioning.

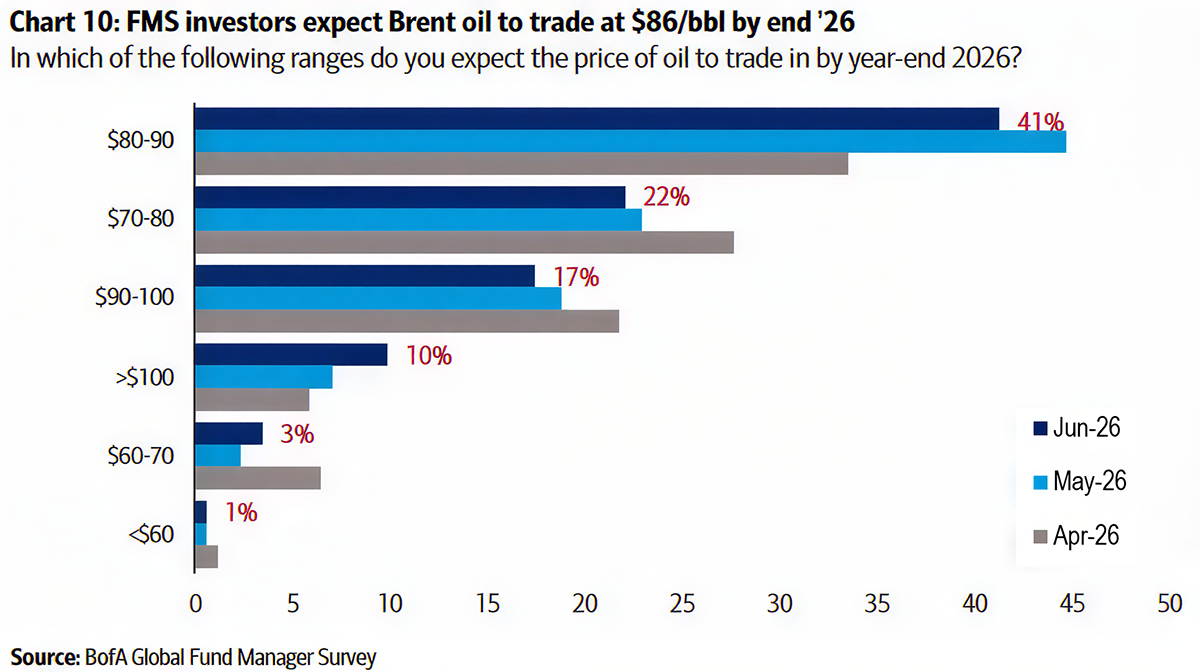

Oil expectations also remain firm: investors expect Brent to trade around $86/bbl by year-end 2026, with 41% looking for $80–90, 17% for $90–100, and 10% above $100. That keeps energy embedded in the inflation story, even as geopolitics has faded as the dominant tail risk. Investors are no longer pricing oil as a full-blown geopolitical panic, but they are also not assuming a quick return to cheap energy.

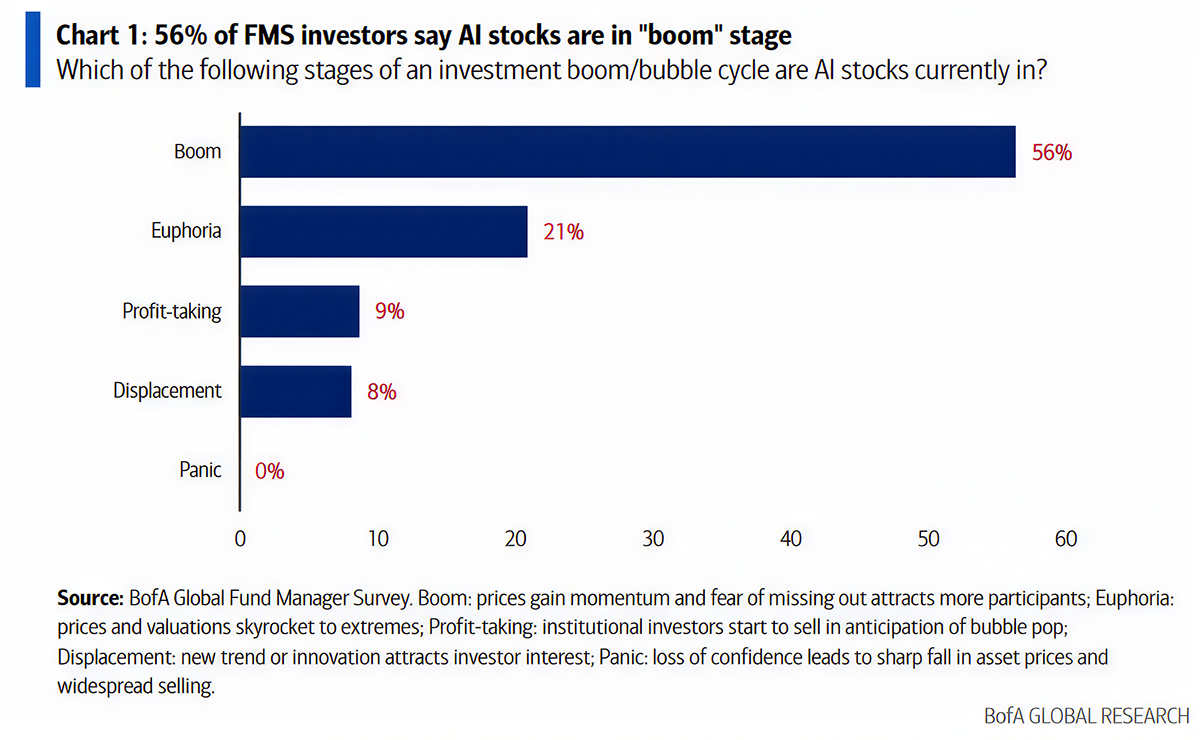

The AI trade remains the clearest source of both optimism and crowding. A majority of investors, 56%, say AI stocks are still in the “boom” phase, where momentum and fear of missing out attract more participants, while only 21% see “euphoria” and just 9% describe the market as already in “profit-taking” mode. That distinction matters: investors are worried about crowding, but most do not yet see AI as being in the final liquidation stage. This is understandable given the scale of the move: at the time the survey was conducted, the PHLX Semiconductor Sector Index was up more than 70% year-to-date. After a rally of that size, the debate naturally shifts from whether the AI cycle is real to whether too much of that future has already been discounted in semiconductor prices.

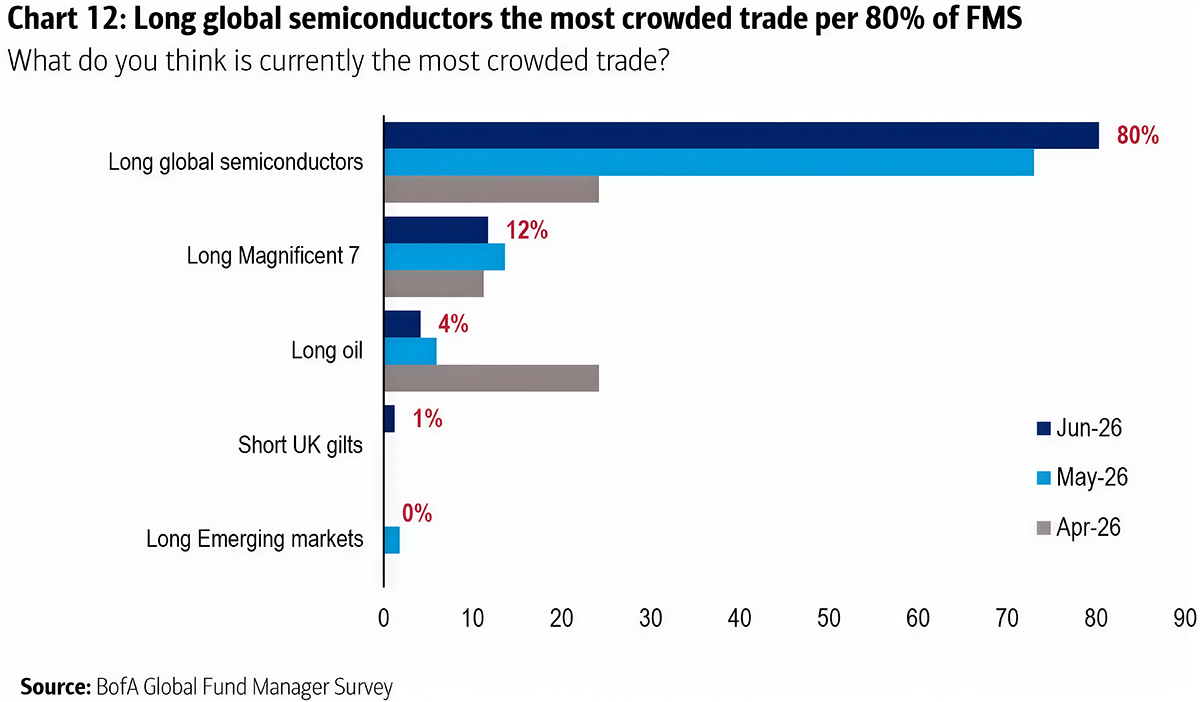

That explains the survey’s central tension: investors still see more runway for the AI theme, but crowding has become extreme. A record 80% identify “long global semiconductors” as the most crowded trade, up from 73% in May, while “long Magnificent 7” is a distant second at 12% and “long oil” has fallen to 4%. The message is clear: this is not broad market euphoria, but a very concentrated form of optimism.

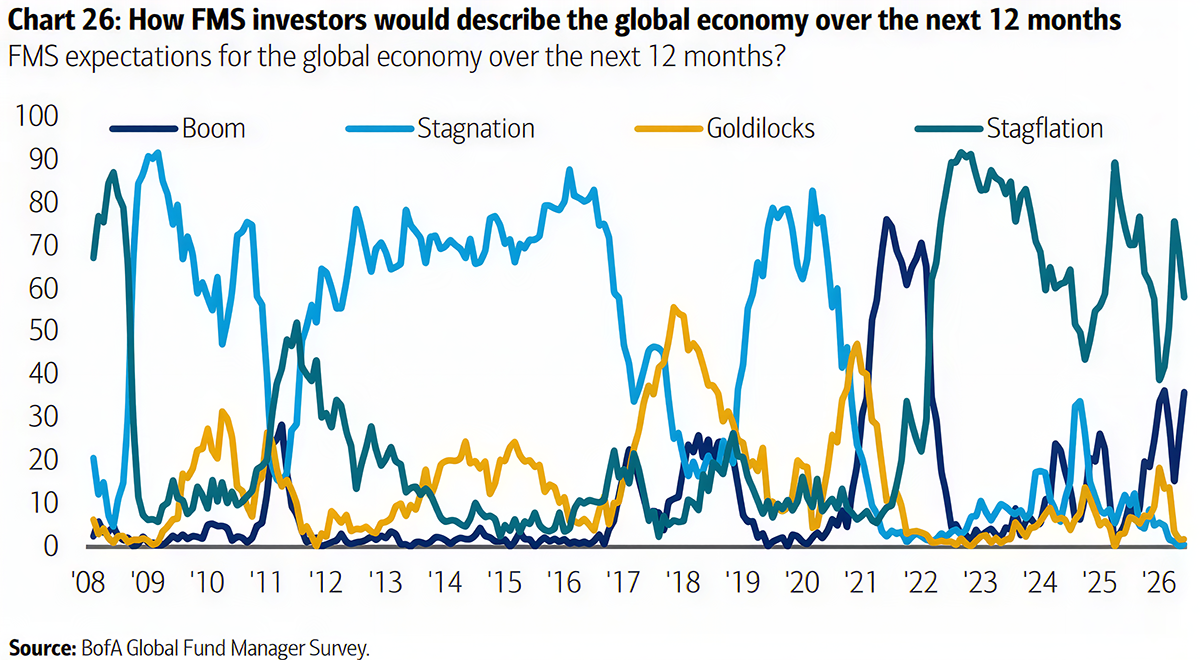

The broader macro distribution also shows that investors are not returning to a classic Goldilocks view. Stagflation remains the dominant description of the next 12 months, cited by 58% of respondents, though down from 69% in May, while the “boom” camp rose to 36% from 25%. Goldilocks remains almost absent at just 2%, and only 1% expect outright stagnation. In other words, investors have become more optimistic on growth, but not because they expect inflation to disappear. The prevailing view is still one of stronger nominal growth accompanied by above-trend inflation.

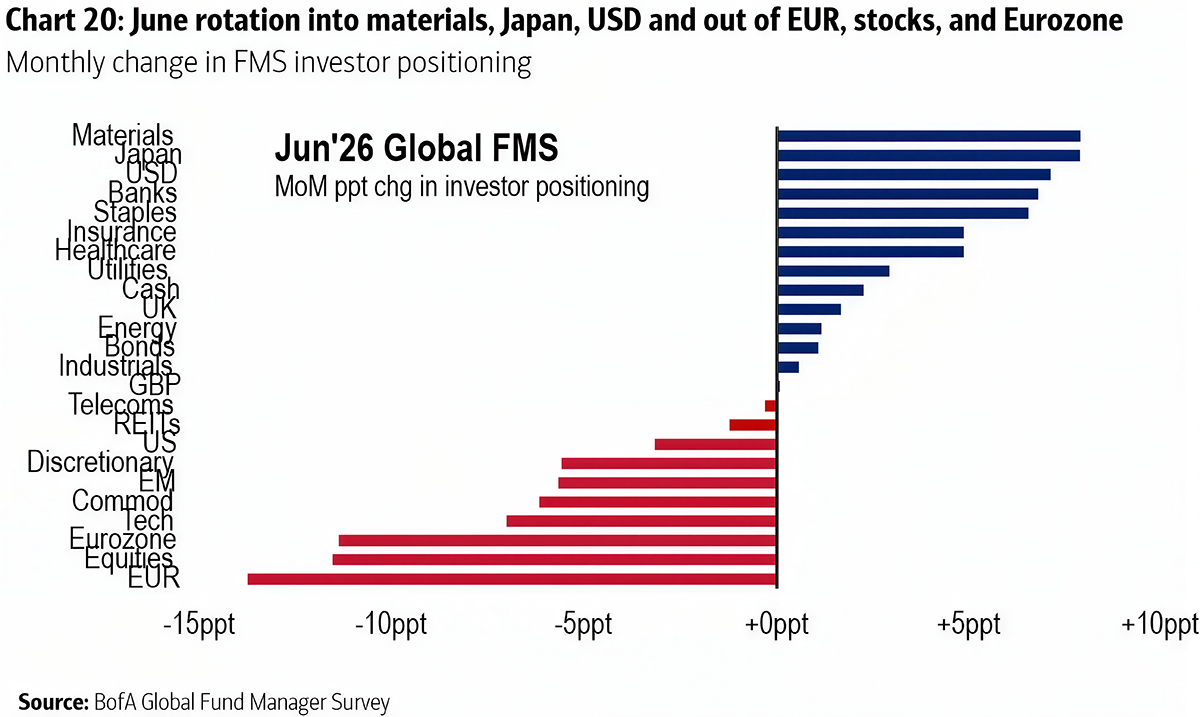

June’s positioning changes show a clear shift from aggressive beta-chasing toward more selective risk-taking. Investors added to materials, banks, Japan, the U.S. dollar and several defensive sectors, while cutting technology, Eurozone equities, commodities, emerging markets and discretionary stocks. The message is not that managers are fleeing risk, but that they are rotating away from the most crowded winners and rebuilding some portfolio balance after May’s one-way chase.

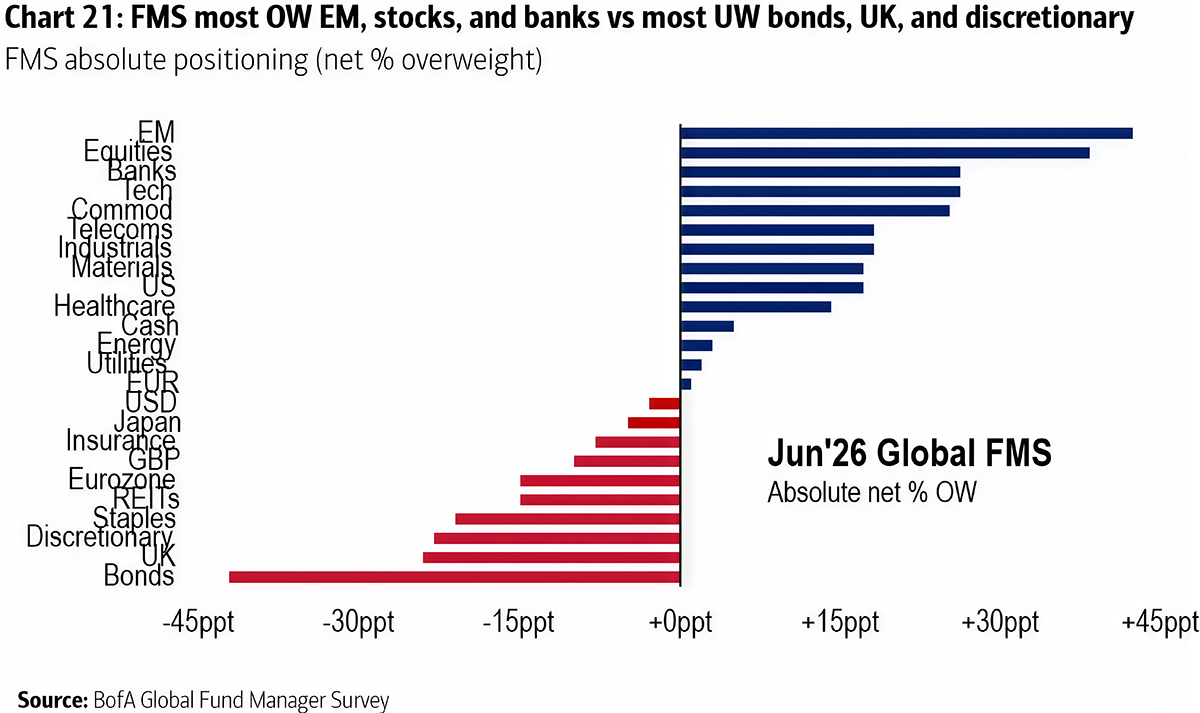

Even after those adjustments, positioning remains clearly pro-risk. Managers are still overweight global equities, emerging markets, technology and commodities, while bonds remain deeply underweight at net -42%. That combination matters: investors are trimming the hottest exposures, but they are not rebuilding a defensive portfolio. They remain positioned for nominal growth, equity leadership and continued pressure on bonds.

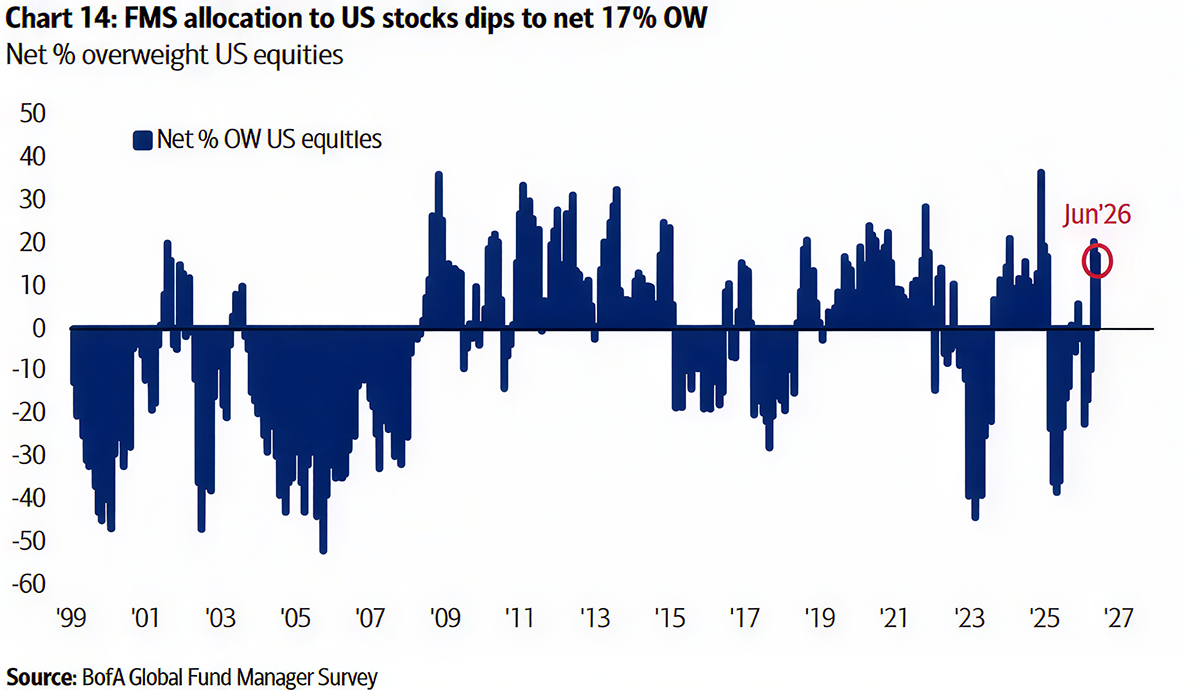

U.S. equity exposure slipped only modestly to a net 17% overweight,

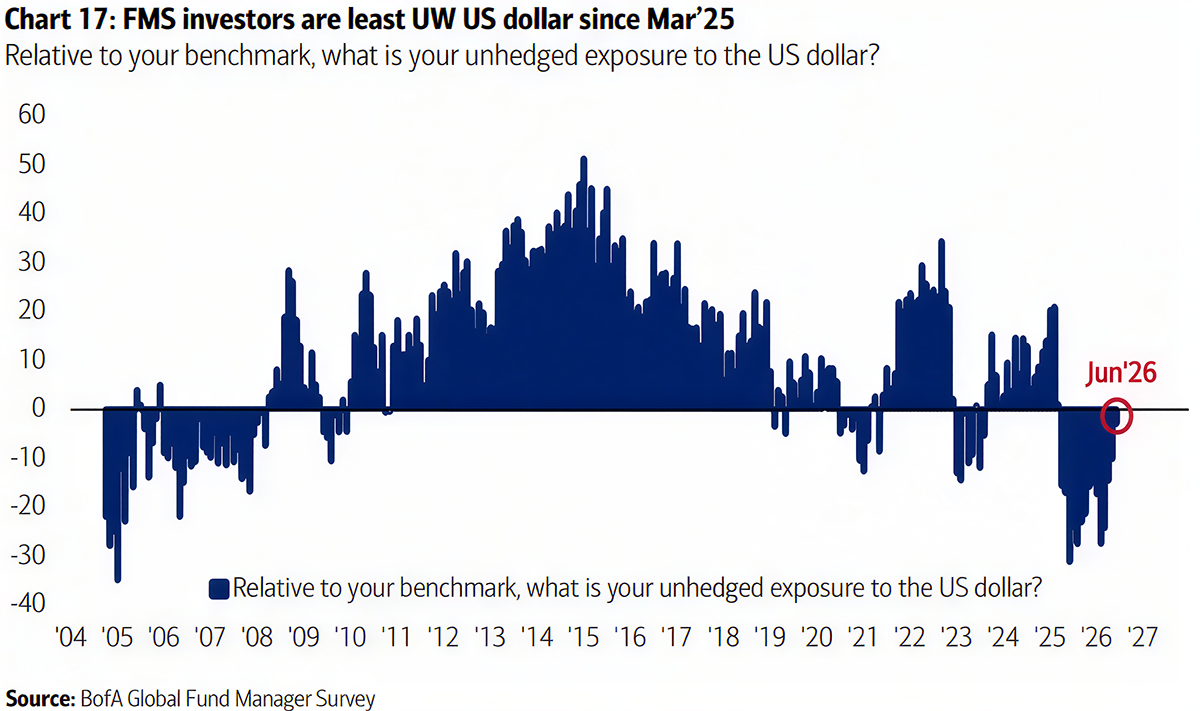

while investors continued to cover U.S. dollar shorts, leaving the currency just 3% underweight, the least negative positioning since March 2025. This reinforces the idea that the U.S. is no longer being treated as a tactical underweight: investors may be trimming some equity exposure, but they are not abandoning U.S. exceptionalism or the dollar hedge against higher rates.

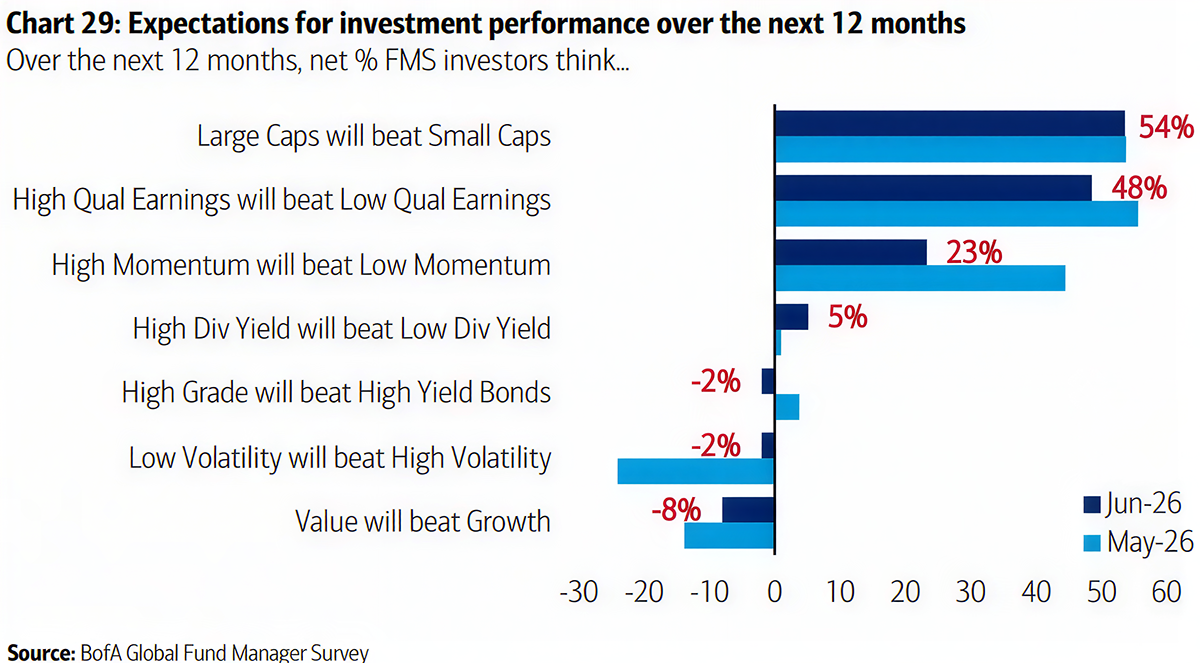

Style preferences confirm that investors still favor market leadership, but with greater selectivity than in May. A net 54% expect large caps to outperform small caps, the strongest conviction among the style factors surveyed, while 48% expect high-quality earnings to outperform low-quality earnings. Momentum remains favored, but much less aggressively, with only 23% expecting high-momentum stocks to outperform, down from 44% in May. Growth also remains preferred over value, though by a narrower margin than a month ago. Together, these results suggest investors continue to favor the AI-led leadership trade, but are becoming less willing to chase momentum indiscriminately.

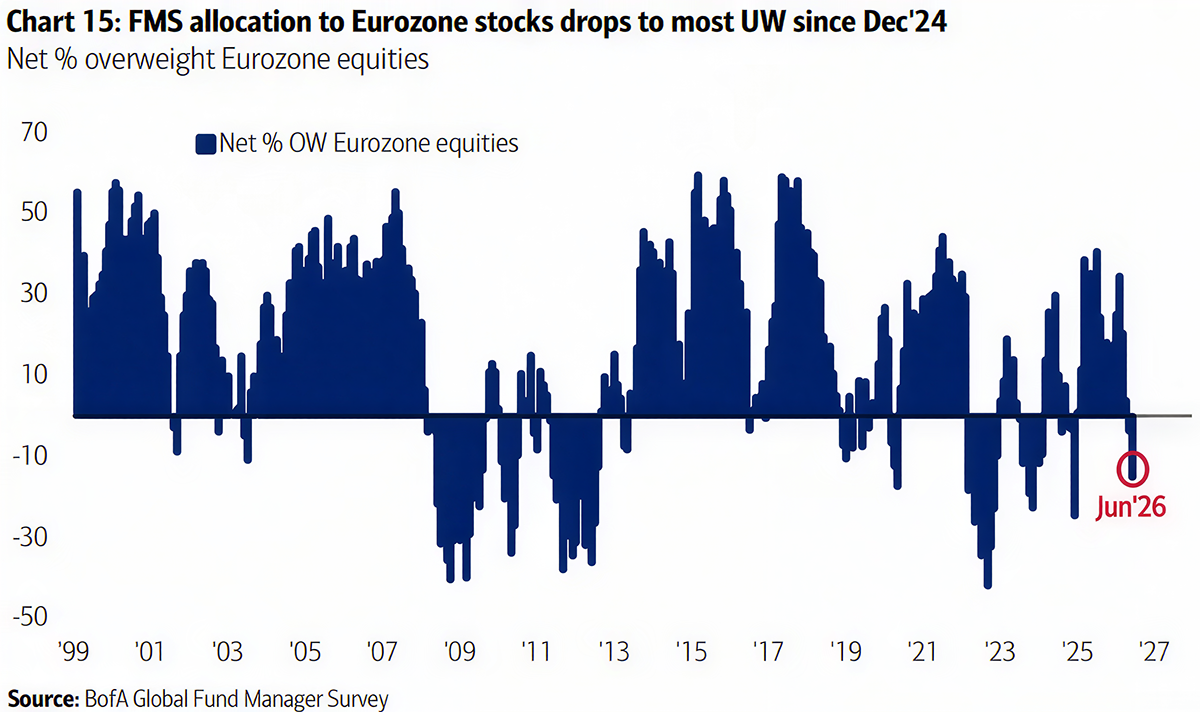

The European picture illustrates this tension. While longer-term confidence has improved materially, with 71% of respondents expecting European equities to rise over the next 12 months and a record 93% expecting forward earnings growth, investors have nevertheless reduced exposure to the region from net -4% to -15% underweight. The survey suggests this reflects relative rather than absolute concerns: 68% now believe U.S. growth and earnings superiority will continue to drive Europe’s structural underperformance, up sharply from 30% in February. In other words, investors have become more optimistic about Europe itself, but even more optimistic about competing opportunities elsewhere.

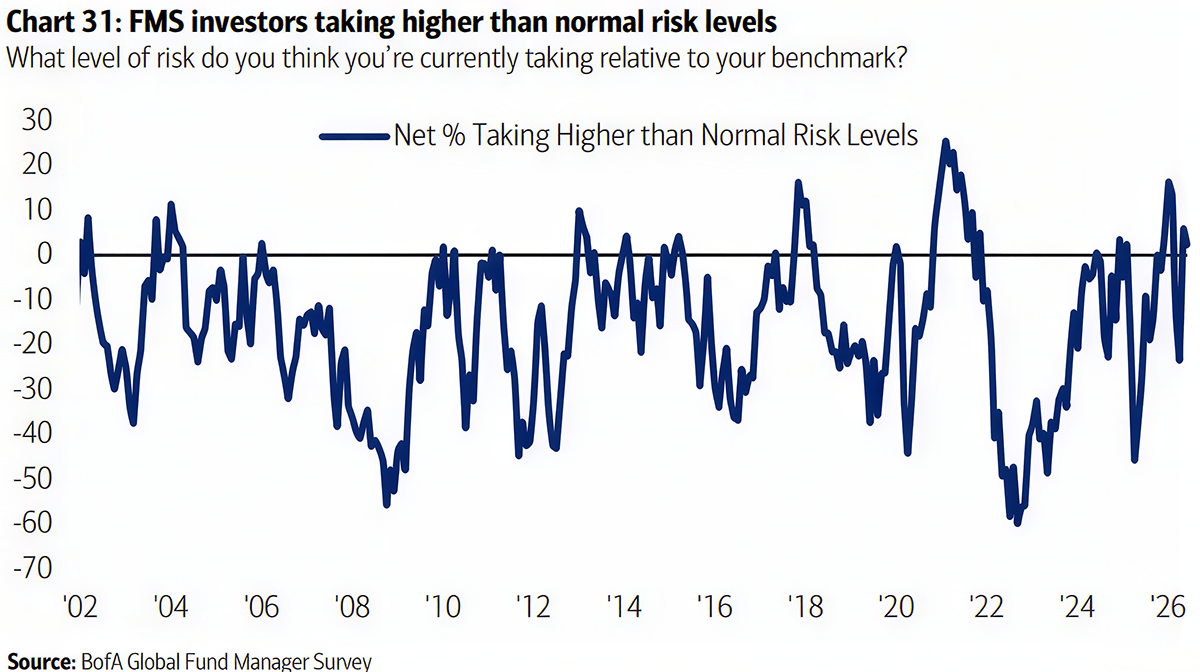

Risk-taking data reinforce the view that June was a moderation rather than a reversal. Investors are still taking net 2% higher-than-normal risk relative to their benchmarks, down from May’s more aggressive stance but no longer below normal levels. That places the survey in a middle ground: managers are not becoming defensive, but the willingness to add risk after the strong rally of recent months has clearly diminished.

Overall, the June survey shows a market that is still bullish, but no longer accelerating in a straight line. Investors remain heavily exposed to equities, AI, semiconductors, emerging markets and U.S. stocks, while cash is still low and bonds remain deeply underowned. At the same time, the risks are becoming more asymmetric: in Hartnett’s June 12 Flow Show, BofA’s Bull & Bear Indicator rose to a sell-signal level of 8.8, while the FMS itself shows semiconductor crowding at an all-time high and rate expectations turning hawkish just as investors still expect growth and profits to improve. The danger is that this has become a narrow consensus: better growth, sticky inflation, higher rates, AI leadership and weak bonds. If any one of those pillars breaks — especially earnings momentum or bond-yield stability — positioning could adjust quickly. The survey’s message is therefore not “risk-off,” but “late-stage risk-on”: markets can still be supported if earnings hold and yields stabilize, but the margin for disappointment has narrowed.

You can find more articles in our Telegram channel at https://t.me/atranicapital_eng

Or you can subscribe to our Weekly market update at https://atranicapital.substack.com/

Or you can subscribe to our Weekly market update at https://atranicapital.substack.com/

You can subscribe to new issues of the Magazine using the form below.