Submit Request

Rest assured, your privacy is paramount to us. The information you provide will be treated with the utmost confidentiality and used exclusively for investment-related communications. We will never share your data with third parties without your consent.

Thank you for considering Atrani Capital for your investment needs. We look forward to connecting with you soon to explore the wealth of opportunities that can benefit us both.

Atrani Monthly magazine

Investors journey - 2, February 2026

Dear friends,

Every year I hear the same thing in the market: “It’s not easy.” And it’s true — the market isn’t simple. But it always feels that way in the moment because we experience emotions. Investing is full of emotions.

Yet when you step back and look at the charts, everything suddenly seems much simpler.

Every year I hear the same thing in the market: “It’s not easy.” And it’s true — the market isn’t simple. But it always feels that way in the moment because we experience emotions. Investing is full of emotions.

Yet when you step back and look at the charts, everything suddenly seems much simpler.

In this issue of our monthly magazine we have two articles.

First one – Atrani ETF Momentum: Turning Market Trends into a Systematic Strategy

Second – Leveraged ETFs: Powerful Tool or Dangerous Toy?

Let's start!

First one – Atrani ETF Momentum: Turning Market Trends into a Systematic Strategy

Second – Leveraged ETFs: Powerful Tool or Dangerous Toy?

Let's start!

Atrani ETF Momentum: Turning Market Trends into a Systematic Strategy

Financial markets are often described as forward-looking and efficient, yet one of the most persistent findings in both academic research and real-world investing is that assets that have performed well in the recent past often continue to outperform, while laggards can remain weak for extended periods. This phenomenon, known as the momentum anomaly, has been documented across equities, bonds, currencies, and commodities, and across nearly all major markets. Unlike short-term price noise or long-term valuation effects, momentum operates on a medium-term horizon — typically months rather than days or decades — and reflects how information and capital actually flow through markets.

Why momentum exists — and why it hasn’t disappeared

Momentum persists because markets are ultimately driven by people and institutions, not equations. When new information emerges — a shift in economic conditions, earnings trends, monetary policy, or technological change — investors rarely adjust instantly or fully. Instead, reactions tend to be gradual and uneven. Some participants respond early, others wait for confirmation, and large institutions often rebalance slowly due to mandates, risk limits, or liquidity constraints. This helps trends develop over time rather than being fully reflected in a single price jump.

Behavioral factors reinforce this process. Investors are prone to underreact to positive surprises, anchoring on prior beliefs, while also hesitating to abandon losing positions. As prices move, performance chasing and benchmark pressure add a second wave of demand, extending trends further. Importantly, momentum does not rely on predicting the future; it reflects the reality that capital reallocates progressively, not instantaneously.

Crucially, momentum has survived decades of awareness because exploiting it requires discipline and emotional restraint. Momentum strategies can underperform during sharp reversals or range-bound markets, and they require selling assets that “feel cheap” and buying those that already look expensive. Many investors find this psychologically difficult to sustain, which helps explain why the anomaly remains present even in highly competitive markets.

Behavioral factors reinforce this process. Investors are prone to underreact to positive surprises, anchoring on prior beliefs, while also hesitating to abandon losing positions. As prices move, performance chasing and benchmark pressure add a second wave of demand, extending trends further. Importantly, momentum does not rely on predicting the future; it reflects the reality that capital reallocates progressively, not instantaneously.

Crucially, momentum has survived decades of awareness because exploiting it requires discipline and emotional restraint. Momentum strategies can underperform during sharp reversals or range-bound markets, and they require selling assets that “feel cheap” and buying those that already look expensive. Many investors find this psychologically difficult to sustain, which helps explain why the anomaly remains present even in highly competitive markets.

Atrani’s philosophy: momentum as a process, not a prediction

Atrani ETF Momentum is built on a simple principle: follow what the market is rewarding and systematically step away from what it is not. The strategy does not forecast macroeconomic outcomes, earnings growth, or valuation normalization. Instead, it uses a rules-based framework to identify areas of persistent relative strength and rotate exposure accordingly.

Implementation matters. Rather than concentrating risk in a single signal or asset class, the strategy is structured as a multi-engine portfolio, where each component captures a different expression of momentum while remaining transparent and repeatable.

Implementation matters. Rather than concentrating risk in a single signal or asset class, the strategy is structured as a multi-engine portfolio, where each component captures a different expression of momentum while remaining transparent and repeatable.

The current portfolio structure

Today, Atrani ETF Momentum is a systematic rotation strategy that consists of three complementary components, each with a clearly defined role and fixed target weight:

1. Core sector rotation (50%)

The backbone of the strategy is a sectoral ETF rotator focused on U.S. equity sectors. This component seeks to capture broad, macro-driven trends — such as leadership shifts linked to the business cycle, interest-rate dynamics, or inflation regimes. Sector momentum tends to be slower-moving and more persistent, making it a stable foundation for the portfolio.

2. Industry ETF rotation (25% total)

This sleeve targets more granular trends where leadership concentrates within specific industries rather than entire sectors. It is split evenly:

Industry coverage in ETFs is still uneven, which affects implementation. Some industries (e.g., software and parts of the digital economy) are structurally concentrated in U.S.-listed companies, while others (e.g., commodities producers and certain industrial supply chains) are more global by nature. Where the ETF market provides clean building blocks, we separate the universe into U.S. and global industry sleeves to broaden opportunity and reduce home bias. However, the number of truly “pure” industry ETFs is limited, and coverage gaps mean the separation cannot be perfect; in some cases, the best available instrument for an industry theme is the same ETF in both sleeves. The objective is not artificial diversification, but to use the best available liquid proxies to express industry momentum when the product set allows it.

1. Core sector rotation (50%)

The backbone of the strategy is a sectoral ETF rotator focused on U.S. equity sectors. This component seeks to capture broad, macro-driven trends — such as leadership shifts linked to the business cycle, interest-rate dynamics, or inflation regimes. Sector momentum tends to be slower-moving and more persistent, making it a stable foundation for the portfolio.

2. Industry ETF rotation (25% total)

This sleeve targets more granular trends where leadership concentrates within specific industries rather than entire sectors. It is split evenly:

- 12.5% U.S. industry ETFs

- 12.5% global industry ETFs

Industry coverage in ETFs is still uneven, which affects implementation. Some industries (e.g., software and parts of the digital economy) are structurally concentrated in U.S.-listed companies, while others (e.g., commodities producers and certain industrial supply chains) are more global by nature. Where the ETF market provides clean building blocks, we separate the universe into U.S. and global industry sleeves to broaden opportunity and reduce home bias. However, the number of truly “pure” industry ETFs is limited, and coverage gaps mean the separation cannot be perfect; in some cases, the best available instrument for an industry theme is the same ETF in both sleeves. The objective is not artificial diversification, but to use the best available liquid proxies to express industry momentum when the product set allows it.

3. Mega-cap leadership rotation (25%)

The final component focuses on rotation among leading mega-cap technology companies. In periods when leadership becomes concentrated — a common feature of late-cycle or innovation-driven environments — a disproportionate share of returns can be generated by a small group of dominant firms. This sleeve is designed to capture that effect systematically, while avoiding long-term attachment to any single name.

The logic behind this design is practical: sector trends can be broad and persistent, while industry and single-stock momentum can be sharper and more episodic— especially when leadership becomes concentrated. That’s why we implement the strategy through liquid ETFs and a small set of highly tradable mega-caps.

The final component focuses on rotation among leading mega-cap technology companies. In periods when leadership becomes concentrated — a common feature of late-cycle or innovation-driven environments — a disproportionate share of returns can be generated by a small group of dominant firms. This sleeve is designed to capture that effect systematically, while avoiding long-term attachment to any single name.

The logic behind this design is practical: sector trends can be broad and persistent, while industry and single-stock momentum can be sharper and more episodic— especially when leadership becomes concentrated. That’s why we implement the strategy through liquid ETFs and a small set of highly tradable mega-caps.

Why implement momentum through ETFs?

ETFs are ideal building blocks for systematic rotation because they provide liquid, transparent exposure to defined segments of the market. In our case, ETFs allow us to express momentum views at multiple levels—broad sectors, targeted industries, and thematic leadership—without needing to constantly pick individual stocks across the entire market. That structure supports discipline: the strategy rotates based on signals rather than narratives, and it avoids holding persistent underperformers simply because they appear “cheap” or familiar.

How the strategy behaves across market regimes

Momentum does not eliminate drawdowns, but it can change where risk comes from by steering exposure toward areas of relative strength. In broad equity selloffs, the strategy typically remains invested in equities, yet it seeks the segments holding up best—illustrated in 2022, when Energy was the only U.S. sector to finish positive and the sector engine rotated into that leadership while the S&P 500 declined -18.1%. In more concentrated markets, performance is often driven by a smaller number of high-conviction positions rather than broad exposure. Historically, individual holdings have at times generated large excess returns versus the benchmark—such as META (+102 percentage points of excess return over a 23-month holding period) and an oil & gas exploration ETF position (XOP, +65 percentage points of excess return over its holding period). The main challenge for momentum tends to be sharp leadership reversals and range-bound, mean-reverting markets, when winners and laggards switch too quickly for trends to be confirmed. This is a known trade-off: the strategy prioritizes robustness and discipline over short-term responsiveness.

For whom this approach makes sense

Atrani ETF Momentum is designed for investors who accept equity-level volatility but want an adaptive alternative to static buy-and-hold allocations. It can be used as a core growth allocation or as a satellite strategy alongside traditional equity exposure. The key benefit is process clarity: investors can understand in advance what the strategy owns, why it rotates, and the market conditions under which it may lag. Rather than forecasting regime changes, it stays focused on aligning with prevailing market leadership through a repeatable, rules-based process.

Closing note

In Issue #1 of Atrani Magazine, we wrote about how investor returns often lag market returns due to poor timing and behavioral mistakes. Atrani ETF Momentum is, in many ways, a direct response to that problem: it is built to replace reactive decision-making with a structured process that systematically follows leadership and exits laggards. The aim is not to predict markets, but to apply a repeatable process that keeps exposure aligned with leadership as it evolves.

Leveraged ETFs: Powerful Tool or Dangerous Toy?

Leveraged ETFs are among the most misunderstood instruments in modern financial markets. They promise magnified returns — but also embed structural risks that many investors underestimate.

Understanding how these products actually work is essential before using them.

Understanding how these products actually work is essential before using them.

What leveraged ETFs are designed to do

Leveraged exchange-traded funds (ETFs) are designed to amplify the daily performance of an underlying index.

Typical structures include:

• 2× ETFs — targeting twice the daily move of an index

• 3× ETFs — targeting three times the daily move

For example, if the S&P 500 rises 1% in a day, a 3× leveraged ETF tracking the index should rise approximately 3% that same day.

If the index falls 1%, the ETF should fall about 3%.

In theory this sounds straightforward: if the S&P 500 rises 10%, a 3× ETF should gain roughly 30%.

In practice the mechanics are more complex. Leveraged ETFs reset their exposure daily, using derivatives such as swaps and futures to maintain a constant leverage ratio. Because of this daily rebalancing, long-term returns do not simply equal the index return multiplied by the leverage factor. The actual outcome depends heavily on volatility and the sequence of daily returns.

This mechanism leads to one of the most misunderstood phenomena in modern ETF investing: volatility decay (sometimes called beta slippage or term decay). In addition to volatility effects, leveraged ETFs also incur financing costs, derivative spreads, and trading frictions, which further reduce long-term returns relative to a simple leveraged benchmark.

Typical structures include:

• 2× ETFs — targeting twice the daily move of an index

• 3× ETFs — targeting three times the daily move

For example, if the S&P 500 rises 1% in a day, a 3× leveraged ETF tracking the index should rise approximately 3% that same day.

If the index falls 1%, the ETF should fall about 3%.

In theory this sounds straightforward: if the S&P 500 rises 10%, a 3× ETF should gain roughly 30%.

In practice the mechanics are more complex. Leveraged ETFs reset their exposure daily, using derivatives such as swaps and futures to maintain a constant leverage ratio. Because of this daily rebalancing, long-term returns do not simply equal the index return multiplied by the leverage factor. The actual outcome depends heavily on volatility and the sequence of daily returns.

This mechanism leads to one of the most misunderstood phenomena in modern ETF investing: volatility decay (sometimes called beta slippage or term decay). In addition to volatility effects, leveraged ETFs also incur financing costs, derivative spreads, and trading frictions, which further reduce long-term returns relative to a simple leveraged benchmark.

The key detail most investors miss: daily rebalancing

The critical feature of leveraged ETFs is that the leverage target applies only to daily returns.

At the end of each trading day, the fund rebalances its exposure to maintain the target leverage ratio.

This daily reset means that over longer periods, returns can deviate significantly from the simple multiple many investors expect.

At the end of each trading day, the fund rebalances its exposure to maintain the target leverage ratio.

This daily reset means that over longer periods, returns can deviate significantly from the simple multiple many investors expect.

Why long-term performance can differ from expectations

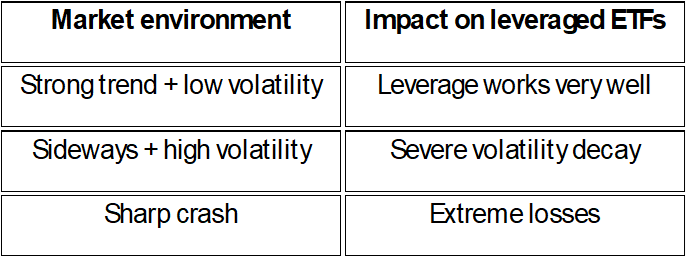

Another important feature of leveraged ETFs is path dependency. Two markets can start and end at the same price but produce very different outcomes for leveraged funds depending on the sequence in which returns occur. A smooth upward trend allows leveraged ETFs to compound gains effectively, while a volatile sideways market forces the fund to repeatedly rebalance — buying after gains and selling after losses — which gradually erodes returns.

Consider a market that repeatedly rises and falls by the same percentage. Even if the underlying asset finishes close to its starting level, the leveraged ETF can gradually lose value because each loss occurs on a larger leveraged base created by the prior gain.

For example:

Index path

+10% → –10%

The index moves:

100 → 110 → 99 (-1%)

But the leveraged ETF declines much more:

100 → 130 → 91 (-9%)

The loss occurs even though the index is nearly flat. This is volatility decay — the destructive compounding effect of alternating gains and losses when leverage is reset daily.

In sideways or highly volatile markets, this effect can significantly reduce long-term returns.

In other words, when markets are highly volatile and returns oscillate up and down, daily rebalancing forces leveraged ETFs into a destructive pattern:

• After gains → leverage is reset from a higher base.

• After losses → leverage is reset from a lower base.

Over repeated cycles this reduces the compounded return relative to the expected leverage factor.

Consider a market that repeatedly rises and falls by the same percentage. Even if the underlying asset finishes close to its starting level, the leveraged ETF can gradually lose value because each loss occurs on a larger leveraged base created by the prior gain.

For example:

Index path

+10% → –10%

The index moves:

100 → 110 → 99 (-1%)

But the leveraged ETF declines much more:

100 → 130 → 91 (-9%)

The loss occurs even though the index is nearly flat. This is volatility decay — the destructive compounding effect of alternating gains and losses when leverage is reset daily.

In sideways or highly volatile markets, this effect can significantly reduce long-term returns.

In other words, when markets are highly volatile and returns oscillate up and down, daily rebalancing forces leveraged ETFs into a destructive pattern:

• After gains → leverage is reset from a higher base.

• After losses → leverage is reset from a lower base.

Over repeated cycles this reduces the compounded return relative to the expected leverage factor.

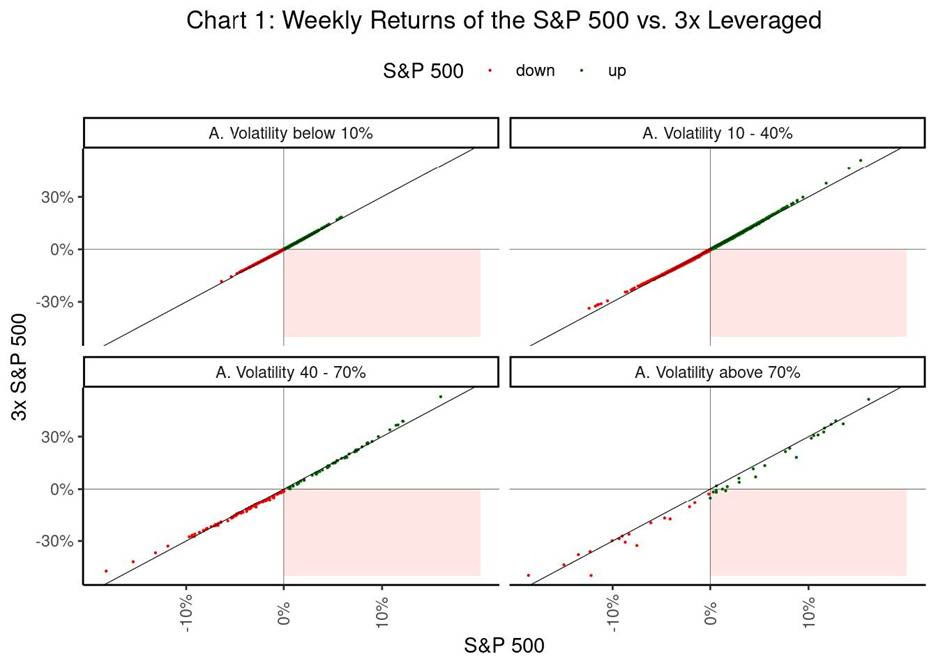

Decay Increases Non-Linearly With Volatility

Research also highlights that volatility alone does not guarantee decay. The key driver is the combination of high volatility and negative serial correlation of returns, which forces leveraged ETFs into a repeated pattern of buying high and selling low during daily rebalancing.

Research by Michael A. Gayed suggests that annualized volatility around 40% becomes an important threshold above which leveraged ETFs tend to systematically underperform their target leverage multiple.

Research by Michael A. Gayed suggests that annualized volatility around 40% becomes an important threshold above which leveraged ETFs tend to systematically underperform their target leverage multiple.

At extremely high volatility levels, the probability of losing money can exceed the probability of gains even when the underlying asset has a positive expected return.

Importantly, volatility decay is not inevitable. The same compounding mechanism that erodes returns in volatile markets can work in the opposite direction during strong trends.

Importantly, volatility decay is not inevitable. The same compounding mechanism that erodes returns in volatile markets can work in the opposite direction during strong trends.

When leveraged ETFs work best

While volatility decay receives much attention, the opposite effect is less discussed.

When markets move consistently in one direction, daily compounding can become beneficial. In strong trends with relatively low volatility, leveraged ETFs may outperform the simple leverage multiple of the index.

The reason is straightforward: consecutive gains increase the capital base from which the next leveraged return is calculated. In trending markets this compounding effect becomes powerful.

Therefore the performance of leveraged ETFs is largely determined by the structure of market returns:

When markets move consistently in one direction, daily compounding can become beneficial. In strong trends with relatively low volatility, leveraged ETFs may outperform the simple leverage multiple of the index.

The reason is straightforward: consecutive gains increase the capital base from which the next leveraged return is calculated. In trending markets this compounding effect becomes powerful.

Therefore the performance of leveraged ETFs is largely determined by the structure of market returns:

This explains why some leveraged ETFs have produced surprisingly strong long-term returns despite their structural risks.

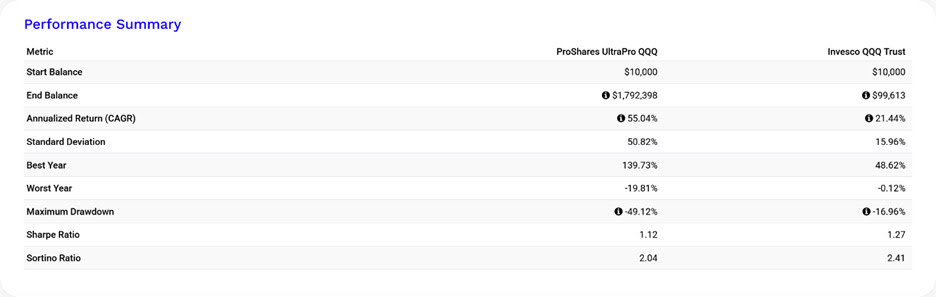

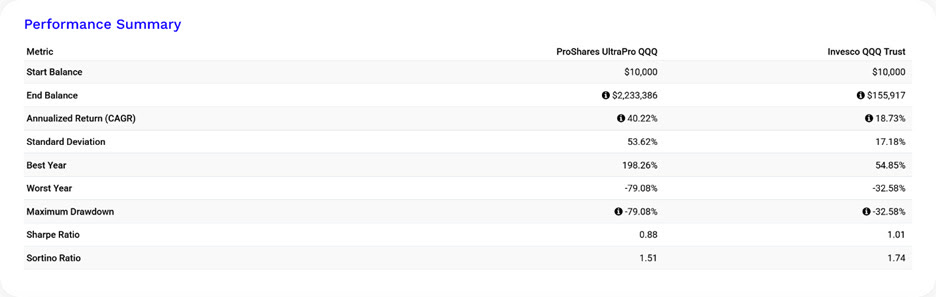

The TQQQ Paradox

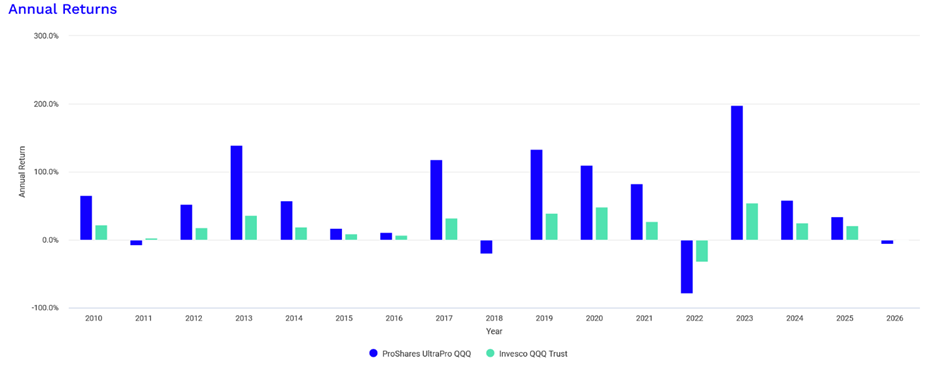

One of the most striking examples is the ProShares UltraPro QQQ (TQQQ), a 3× leveraged ETF tracking the Nasdaq-100.

According to conventional wisdom, leveraged ETFs should perform poorly over long horizons due to volatility decay. Yet since its launch in 2010, TQQQ has produced extraordinary cumulative returns — at times even exceeding three times the performance of the Nasdaq-100.

This apparent paradox can be explained by the market environment of the past decade.

Between 2010 and 2021, U.S. technology stocks experienced:

• a persistent upward trend,

• relatively moderate volatility,

• long streaks of positive returns.

These conditions are precisely those in which leveraged compounding becomes favorable. As a result, TQQQ benefited from positive compounding rather than decay, turning leverage into a powerful amplifier of the long technology bull market.

Even in an exceptionally favorable environment, TQQQ did not deliver a constant 3× multiple over the long run.

According to conventional wisdom, leveraged ETFs should perform poorly over long horizons due to volatility decay. Yet since its launch in 2010, TQQQ has produced extraordinary cumulative returns — at times even exceeding three times the performance of the Nasdaq-100.

This apparent paradox can be explained by the market environment of the past decade.

Between 2010 and 2021, U.S. technology stocks experienced:

• a persistent upward trend,

• relatively moderate volatility,

• long streaks of positive returns.

These conditions are precisely those in which leveraged compounding becomes favorable. As a result, TQQQ benefited from positive compounding rather than decay, turning leverage into a powerful amplifier of the long technology bull market.

Even in an exceptionally favorable environment, TQQQ did not deliver a constant 3× multiple over the long run.

Including the most recent market cycles further illustrates the divergence between leveraged and unleveraged returns. Over the full period, the effective leverage multiple falls to roughly 2.1×. At the same time, volatility increases disproportionately, which reduces the Sharpe ratio — meaning that risk rises faster than return.

However, this outcome should not be interpreted as evidence that leveraged ETFs are suitable for long-term buy-and-hold investing. The same mechanism that boosted returns in a strong trend can quickly work in reverse during volatile downturns.

Long-term investors are often surprised by the magnitude of volatility drag. For example, in 2018 TQQQ lost 19.8% while QQQ was roughly flat. In contrast, during the strong technology rally of 2023 TQQQ surged 198.3% versus 54.9% for QQQ, illustrating how declining volatility and persistent trends can dramatically amplify leveraged returns.

Long-term investors are often surprised by the magnitude of volatility drag. For example, in 2018 TQQQ lost 19.8% while QQQ was roughly flat. In contrast, during the strong technology rally of 2023 TQQQ surged 198.3% versus 54.9% for QQQ, illustrating how declining volatility and persistent trends can dramatically amplify leveraged returns.

Despite the drag from volatility decay, leveraged ETFs can deliver extraordinary long-term returns if the underlying asset experiences a strong, persistent trend with positive serial correlation — conditions that characterized the Nasdaq-100 over much of the past decade.

The key lesson is simple:

Volatility — not time — determines the long-term outcome of leveraged ETFs.

The key lesson is simple:

Volatility — not time — determines the long-term outcome of leveraged ETFs.

The Rise of Single-Stock Leveraged ETFs

The leveraged ETF universe has evolved rapidly in recent years. Until recently, most products tracked broad indexes such as the S&P 500 or Nasdaq-100. That changed in 2022 with the introduction of leveraged single-stock ETFs.

These funds offer 2× or 3× daily exposure to individual stocks such as Tesla, Nvidia, or Apple. By early 2026, more than 300 such products were trading in the US, with total assets exceeding $25 billion.

The appeal is clear: investors can obtain leveraged exposure to popular stocks without using margin accounts or derivatives.

However, research suggests the risks may be even greater than for index-based leveraged ETFs.

A study by Hendrik Bessembinder found that leveraged single-stock ETFs underperform their theoretical leverage benchmark by roughly 0.8% per month on average, with roughly one-third of the underperformance caused by daily rebalancing effects and the remainder by transaction and financing frictions.

Bessembinder’s analysis highlights a deeper structural property of leveraged strategies. When returns are volatile and exhibit mean-reversion, maintaining constant leverage forces the strategy to systematically buy after price increases and sell after declines, generating negative compounding effects. Over time this mechanical rebalancing creates a persistent performance gap between leveraged ETFs and a simple leveraged buy-and-hold benchmark.

Because individual stocks are typically far more volatile than diversified indexes, volatility decay can become significantly more severe in single-stock leveraged ETFs.

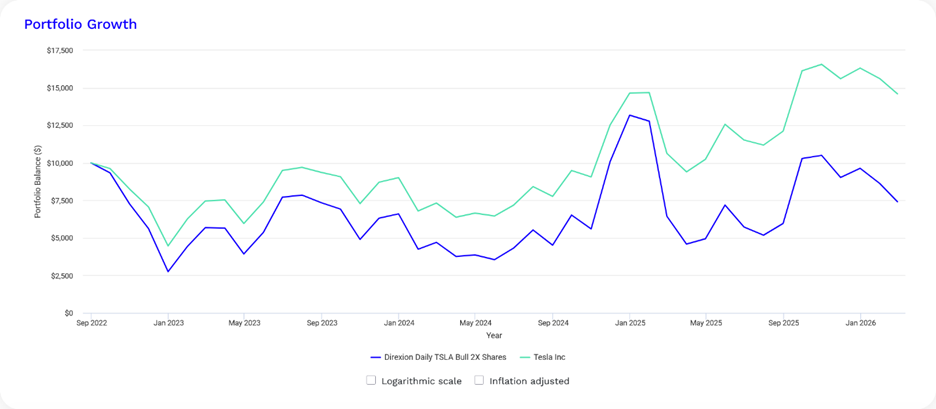

The chart below compares Tesla shares with the Direxion Daily TSLA Bull 2× ETF over the same period. While Tesla’s stock eventually recovered after several drawdowns, the leveraged ETF failed to keep pace with the underlying stock.

Even though the fund targets twice Tesla’s daily return, the long-term result is significantly worse than simply holding the stock. The reason is the same path-dependency mechanism described earlier: Tesla’s large price swings force the ETF to rebalance exposure repeatedly, locking in losses during volatile periods.

These funds offer 2× or 3× daily exposure to individual stocks such as Tesla, Nvidia, or Apple. By early 2026, more than 300 such products were trading in the US, with total assets exceeding $25 billion.

The appeal is clear: investors can obtain leveraged exposure to popular stocks without using margin accounts or derivatives.

However, research suggests the risks may be even greater than for index-based leveraged ETFs.

A study by Hendrik Bessembinder found that leveraged single-stock ETFs underperform their theoretical leverage benchmark by roughly 0.8% per month on average, with roughly one-third of the underperformance caused by daily rebalancing effects and the remainder by transaction and financing frictions.

Bessembinder’s analysis highlights a deeper structural property of leveraged strategies. When returns are volatile and exhibit mean-reversion, maintaining constant leverage forces the strategy to systematically buy after price increases and sell after declines, generating negative compounding effects. Over time this mechanical rebalancing creates a persistent performance gap between leveraged ETFs and a simple leveraged buy-and-hold benchmark.

Because individual stocks are typically far more volatile than diversified indexes, volatility decay can become significantly more severe in single-stock leveraged ETFs.

The chart below compares Tesla shares with the Direxion Daily TSLA Bull 2× ETF over the same period. While Tesla’s stock eventually recovered after several drawdowns, the leveraged ETF failed to keep pace with the underlying stock.

Even though the fund targets twice Tesla’s daily return, the long-term result is significantly worse than simply holding the stock. The reason is the same path-dependency mechanism described earlier: Tesla’s large price swings force the ETF to rebalance exposure repeatedly, locking in losses during volatile periods.

In other words, higher volatility increases the gap between leveraged products and their theoretical leverage multiple — a problem that becomes particularly pronounced when leverage is applied to individual stocks rather than diversified indexes.

The Industry Keeps Pushing the Limits

Despite the structural risks, demand for leveraged ETFs continues to grow rapidly.

In fact, leveraged and inverse ETFs represent only a small share of total ETF assets but account for a disproportionately large share of industry revenues and trading volumes.

According to Bloomberg Intelligence estimates, leveraged ETFs generated roughly $1 billion in annual revenue, despite representing only a small fraction of the overall ETF market. High fees combined with strong trading activity make them extremely profitable products for issuers.

Competition among ETF providers has led to increasingly aggressive product designs. In 2025 several firms — including ProShares, Direxion, GraniteShares and Volatility Shares — submitted filings for 3× and even 5× leveraged ETFs, targeting assets ranging from the Nasdaq-100 to individual stocks and cryptocurrencies.

Regulators have begun pushing back. In early 2026 the SEC asked issuers not to proceed with launching several ultra-leveraged ETFs, citing concerns about compliance with derivatives risk rules under Rule 18f-4.

Recent events have already illustrated the dangers.

In October 2025, a 3× inverse AMD ETP listed in Europe collapsed to zero after AMD shares surged roughly 38%, forcing the issuer to close the product. Investors received no redemption payments after the fund’s net asset value was wiped out.

The episode highlighted a structural risk of highly leveraged single-stock products: large price moves in the underlying asset can rapidly destroy the fund’s value.

In fact, leveraged and inverse ETFs represent only a small share of total ETF assets but account for a disproportionately large share of industry revenues and trading volumes.

According to Bloomberg Intelligence estimates, leveraged ETFs generated roughly $1 billion in annual revenue, despite representing only a small fraction of the overall ETF market. High fees combined with strong trading activity make them extremely profitable products for issuers.

Competition among ETF providers has led to increasingly aggressive product designs. In 2025 several firms — including ProShares, Direxion, GraniteShares and Volatility Shares — submitted filings for 3× and even 5× leveraged ETFs, targeting assets ranging from the Nasdaq-100 to individual stocks and cryptocurrencies.

Regulators have begun pushing back. In early 2026 the SEC asked issuers not to proceed with launching several ultra-leveraged ETFs, citing concerns about compliance with derivatives risk rules under Rule 18f-4.

Recent events have already illustrated the dangers.

In October 2025, a 3× inverse AMD ETP listed in Europe collapsed to zero after AMD shares surged roughly 38%, forcing the issuer to close the product. Investors received no redemption payments after the fund’s net asset value was wiped out.

The episode highlighted a structural risk of highly leveraged single-stock products: large price moves in the underlying asset can rapidly destroy the fund’s value.

Why Leveraged ETFs Keep Attracting Investors

Despite the well-documented effects of volatility decay, path dependency, and periodic product failures, leveraged ETFs continue to grow rapidly.

The explanation lies in a combination of market structure, investor behavior, and the unique payoff profile these products offer.

First, leveraged ETFs provide easy access to leverage without margin accounts or derivatives. Retail investors can obtain amplified exposure to an index or a single stock simply by purchasing an ETF, avoiding the operational complexity of futures, swaps, or borrowing. This accessibility dramatically expands the potential user base.

Second, the products are designed primarily for short-term trading rather than long-term investing. Many traders use leveraged ETFs tactically to express directional views over hours or days. In such short horizons, volatility decay is typically negligible, while the leverage allows investors to deploy smaller amounts of capital to achieve meaningful exposure.

Third, leveraged ETFs offer highly convex payoff profiles in strong trends. When markets rise steadily with relatively low volatility, the daily compounding mechanism can work in investors’ favor. The experience of funds like the 3× Nasdaq-100 ETF TQQQ during the technology bull market illustrates this dynamic: persistent upward trends can generate extraordinary returns despite the theoretical drag from daily rebalancing.

Finally, there are strong incentives on the supply side. Leveraged ETFs typically charge higher fees than traditional index funds, and trading activity in these products tends to be intense. As a result, even though leveraged ETFs represent only a small share of the ETF universe, they generate disproportionately large revenues for issuers. This commercial success encourages providers to continue launching new products and pushing the boundaries of leverage.

The explanation lies in a combination of market structure, investor behavior, and the unique payoff profile these products offer.

First, leveraged ETFs provide easy access to leverage without margin accounts or derivatives. Retail investors can obtain amplified exposure to an index or a single stock simply by purchasing an ETF, avoiding the operational complexity of futures, swaps, or borrowing. This accessibility dramatically expands the potential user base.

Second, the products are designed primarily for short-term trading rather than long-term investing. Many traders use leveraged ETFs tactically to express directional views over hours or days. In such short horizons, volatility decay is typically negligible, while the leverage allows investors to deploy smaller amounts of capital to achieve meaningful exposure.

Third, leveraged ETFs offer highly convex payoff profiles in strong trends. When markets rise steadily with relatively low volatility, the daily compounding mechanism can work in investors’ favor. The experience of funds like the 3× Nasdaq-100 ETF TQQQ during the technology bull market illustrates this dynamic: persistent upward trends can generate extraordinary returns despite the theoretical drag from daily rebalancing.

Finally, there are strong incentives on the supply side. Leveraged ETFs typically charge higher fees than traditional index funds, and trading activity in these products tends to be intense. As a result, even though leveraged ETFs represent only a small share of the ETF universe, they generate disproportionately large revenues for issuers. This commercial success encourages providers to continue launching new products and pushing the boundaries of leverage.

Who Should Use Leveraged ETFs?

Leveraged ETFs are best understood as short-term tactical instruments, not long-term investment vehicles.

They can be useful for:

• tactical market positioning,

• short-term trading strategies,

• hedging,

• amplifying high-conviction trades.

However, they require careful risk management and a clear understanding of how volatility and compounding affect performance.

For long-term investors, the combination of volatility decay and amplified drawdowns can create outcomes very different from the expected leverage multiple.

For example, a 3× leveraged ETF becomes mathematically impossible to maintain if the underlying asset falls more than 33% in a single day, because the target return would exceed –100%.

They can be useful for:

• tactical market positioning,

• short-term trading strategies,

• hedging,

• amplifying high-conviction trades.

However, they require careful risk management and a clear understanding of how volatility and compounding affect performance.

For long-term investors, the combination of volatility decay and amplified drawdowns can create outcomes very different from the expected leverage multiple.

For example, a 3× leveraged ETF becomes mathematically impossible to maintain if the underlying asset falls more than 33% in a single day, because the target return would exceed –100%.

Conclusion

Leveraged ETFs are best understood as a daily‑reset derivatives wrapper, not as “index investing with a turbo button.” Over multi‑week horizons, outcomes are path dependent: in smooth uptrends, compounding can look miraculous (the TQQQ paradox); in volatile, mean‑reverting regimes, the same daily reset turns into term decay and can leave investors with returns that fall far short of the headline multiple. Academic work emphasizes that the drag is not simply “volatility” — it is volatility interacting with serial dependence, frictions, and rebalancing trades, which is why single‑stock leveraged ETFs have shown systematic shortfalls versus simple leverage benchmarks. That is also why blowups are possible in extreme moves, as the AMD inverse‑3× wipeout illustrated.

The practical recommendation is straightforward. Retail investors should treat leveraged ETFs as short‑duration tools (days, not quarters), size them as overlays, and avoid concentrated 3× single‑stock exposure where gap risk can take NAV to zero. Institutions can use leveraged ETFs as implementation vehicles, but only if they are governed like any derivatives book: regime‑aware stress tests, explicit VaR budgeting under Rule 18f‑4’s limits, liquidity plans, and a pre‑committed unwind protocol when volatility spikes or the thesis breaks.

Leveraged ETFs are powerful financial instruments — but they are not simple investments. Their behavior is governed not just by market direction, but by volatility, path dependency, and the mechanics of daily rebalancing. Leverage magnifies not only returns, but also the consequences of market structure. Investors who understand this dynamic can use leveraged ETFs effectively; those who ignore it may discover that time and volatility are powerful adversaries.

The practical recommendation is straightforward. Retail investors should treat leveraged ETFs as short‑duration tools (days, not quarters), size them as overlays, and avoid concentrated 3× single‑stock exposure where gap risk can take NAV to zero. Institutions can use leveraged ETFs as implementation vehicles, but only if they are governed like any derivatives book: regime‑aware stress tests, explicit VaR budgeting under Rule 18f‑4’s limits, liquidity plans, and a pre‑committed unwind protocol when volatility spikes or the thesis breaks.

Leveraged ETFs are powerful financial instruments — but they are not simple investments. Their behavior is governed not just by market direction, but by volatility, path dependency, and the mechanics of daily rebalancing. Leverage magnifies not only returns, but also the consequences of market structure. Investors who understand this dynamic can use leveraged ETFs effectively; those who ignore it may discover that time and volatility are powerful adversaries.

You can find more articles in our Telegram channel at https://t.me/atranicapital_eng

Or you can subscribe to our Weekly market update at https://atranicapital.substack.com/

Or you can subscribe to our Weekly market update at https://atranicapital.substack.com/

You can subscribe to new issues of the Magazine using the form below.